The only thing we learnt from history was that *we learn nothing from the history*.

For the past decades, what were the central banks all over the world doing? Nothing but printing money. Whenever there was a (economical) crisis, the only measure was printing money, *nothing but printing money*. Were the problems resolved ever? Never!!. They event pretended to be innocent by asking "why there were no inflation". Of course, there was no inflation as the design of CPI, the indicator of indicator, was flawed. CPI does not consider price of assets, otherwise sky would be the limit. There were crisis simply because the money went to the people who didn't it that much. Printing much made things worse as most of the printed money went to those didn't need it much, but nonetheless had postponed them a lot.

Such pretending to be dumb game could have being played a lot longer if not the pandemic which made them had no choice but printing money and sending them to those in need. And all of a sudden, those who needed the money most had so much cash they had never imaged before? What were they going to do? For sure spending them all.

Now here is the long *expected* inflation, what are central banks planning to deal with it? Increasing interest rate to where it should be? Seems too hard, let's print more money!

Central banks have one universal lever, and they use it. (This is by design, so it can be mostly independent.) The responsibility is on the fiscal side to spend it on shit that actually matters.

Sending people money without means testing is dumb, but politics in this age is dumb.

Unfortunately harping half-truths about central banking won't help with the situation :/

Your comment completely ignores the supply side of inflation, ie. food & energy prices. Ie. there's a war between the food and fossil faucets of Europe.

See also the whole baby formula debacle (sustained government intervention reduced the market to a very fragile one, and lobbying and protectionism prevents imports to the US), see the perverse incentives in low-paying logistics sectors (the big ports are all owned by local governments, and they are shit at responding to supply-and-demand, and trucking is of course completely fucked because the liability is shifted to the drivers while the profit is nicely shifted off of their hands, due to a relative large pool of potential new drivers to fleece).

Most of the spike in energy costs for the consumers is caused primarily by how energy markets are designed, not by hikes in gas prices (which could only justify a small part of the price hike).

See this long, but well explained, video on the topic [0].

Neglecting issues due to the war in Ukraine, a lot of the “supply side issues” are not totally isolated from central bank policy, QE, and stimulus. The use of QE and stimulus increased demand, while simultaneously, government policy decreased supply. Now, supply is (mostly) recovered, but demand still remains elevated. Supply can’t keep up, because its target is too high.

This is why we see talk from the Federal Reserve about how consumers will “feel pain” - the only way to reduce demand is to reduce employment or wages, to a level that the supply chain is capable of keeping up with. The Fed press conferences are really interesting to watch as they make this very clear - we are really looking at an “imbalance between supply and demand” due in part to all of economic, social, and political factors.

Also, regarding the CPI not reflecting asset prices: the CPI does not include any measure of equity prices, for instance. Since so many rely on equities to fund their retirement, an increase in equity prices is a meaningful inflation. If the price of the S&P 500 for instance is higher due to an asset bubble, it decreases my ability to purchase shares of it. The increase in equity prices we see is really inflation of equities, but never branded as such. We call it “return on investment”, because the people talking about it are mostly those who already own equities, not those looking to buy them. It’s the same reason as why homeowners dislike seeing home prices increase, while homebuyers enjoy it.

I’ll also mention that the CPI has a lot of other bunk practices in it. For instance, “hedonistic adjustment”. A (slightly conspiratorial) site called ShadowStats computes a modified CPI that uses older CPI methodology (before the meaning of inflation was redefined to show lower inflation) that currently sits at 17 or so percent.

> If the price of the S&P 500 for instance is higher due to an asset bubble, it decreases my ability to purchase shares of it.

BLS says that the CPI doesn't track savings, just day-to-day living expenses. And that's okay, people want these indices to do everything. (And the Fed is not even using the CPI, they are using the PCE ... and there's a bunch more https://www.bea.gov/resources/learning-center/quick-guide-so... And the PCE is considered too broad, because it has inputs from businesses, nonprofits, etc. But of course it's not like business costs are irrelevant to the economy...)

That said, I think the biggest problem is that these general indices are used for things like welfare calculations, but they already don't represent the average welfare recipient. So adding equity would make it even less useful for that. (Which is mostly just an argument for having more indices, each representing a large chunk of society. But of course the cynic in me says that we already have one for the important people, the SP500, and poor people only matter when they are undecided voters in swing states.)

> Now, supply is (mostly) recovered, but demand still remains elevated.

Mostly, though basic input like oil is still not at the early 2020 levels. Aaand OPEC cut production just yesterday.

> we are really looking at an “imbalance between supply and demand” due in part to all of economic, social, and political factors.

Yep. And every think tank from the political zoo has their own critique of the actions of the Fed, but monetary policy is simply a blunt tool, and all of the structural problems are ... surprise surprise ... structural conflicts between big powerblocks. (One common laughing stock is the Jones Act. US shipbuilding is basically non-existent, and what's left is useless for "national security" purposes anyway. But it's somehow completely entrenched. Similarly other protectionist policies that serve special interests serve exactly one purpose to enrich members of those special interest groups. It's bad for consumers, it's bad for the economy, it's bad for labor markets, etc.)

All in all there's an argument in this about how the US fucked up the transition during globalization. (The big one is using market access as a carrot in WTO, but then not enforcing reciprocity with China and others. And the lack of any real and effective management of wage deflation in the affected areas, like the rust belt, goes without saying.)

This is clearly an oversimplification because the crisis of 2008 was met with extreme money printing which did not cause a burst of inflation and was reeled in with relative ease as the economy restored itself. If money printing were the variable then it should cause inflation every time but it does not.

I think the GP is saying, 2008's money printing did cause a burst of inflation in stocks, which would have otherwise fallen even further. Measuring CPI by excluding assets like growth stocks hides the true effect of this money printing by glossing over what most already wealthy spend money on.

The extreme money printing (look at the Fed's balance sheet before and after 2008 [0]) showed up as inflation in house prices, which have ballooned in relation to wage income. This was done for the explicit purpose of keeping the biggest lenders flush (see Timothy Geithner's comments about 'deeply unfair', e.g. [1]) and is exactly what the GP is describing.

> because the crisis of 2008 was met with extreme money printing which did not cause a burst of inflation

The inflation was very much visible in the places where the people who received the money spend their money (i.e. Wall Street). The money never made its way to Main Street, so naturally there would be no price pressure found there.

This time around the money was distributed to Main Street.

The money printing in 2008/9 was in response to a deflationary spiral. It didn’t cause inflation because it was mopped up by the deflationary conditions.

At this point the fed seems to be saying that those days are over, they will continue to increase rates until inflation hits 2%. Obviously this cannot go on forever because it becomes impossible to service the debt and you have to print money to pay it off. But it gives you more time and prevents hyper-inflation and we can hope that by then AI and other technological advances have made what we consider "economics" mostly irrelevant.

A company borrowing money to buy back stock sounds like me borrowing money to go on vacation. Rates are cheap, its a no-brainer right? Government will anyway bail me out as soon as a crisis hits, right?

>we can hope that by then AI and other technological advances have made what we consider "economics" mostly irrelevant.

Is there a serious hope that AGI will invent a replicator soon after coming online? It seems likeliest to me that if a greater-than-human intelligence comes online it won't have a circumvention for the laws of thermodynamics and there still won't be such a thing as a free lunch.

No replicator, just extremely cheap labor and energy. Imagine if someone from 1000 years ago could have access to an American garbage dump. Things that in our current economy have zero or negative value would be extremely valuable to those people (Plastics, Metals, Electronics, Machined Clothes, Plant Seeds)

That same thing will happen again once we have another huge advancement in technology. What we consider to be expensive and valuable today will be of zero or negative value to someone 100 years from now.

The 1974 and 1980 peaks from the article correspond to the steeper slope regions in those same years on my graph. (I'm plotting 1/[CPI-U price level], while the article is plotting d/dt [CPI-U price level])

On my y-axis is the purchasing power of a US dollar, relative to current level. So when the y-axis shows 9.813 on 1962-10-04, this means that sixty years ago, a one-dollar bill would buy a basket of goods that today would cost $9.813.

It certainly "feels scary" when the purchasing power is eroding quickly (i.e. a fast-declining slope on my purchasing power graph, or a peak on the article's year-over-year derivative graph).

I haven't dug into everything you are doing, but the biggest flaw I see seems to be that you assume Cash returns 0% nominal, i.e. that there is no return for holding cash. That is only true if you hide it under your mattress(and no deflation happens). Most people do not hide money under their mattress anymore, especially if they have large amounts of it. They put it in a bank account or in a MMF or some other interest producing place.

Since 1972, Cash has a real return of 0.53% (inflation adjusted):

Is that surprising? Alternatively, do you have a fix in mind? Having power means you can build more things that give you more power faster than someone with less power. You can't change this using inflation, as people will just hold something else instead of cash (and, in fact, inflation seems to most punish the people with the least power, as those people are spending a much much greater proportion of their income on critical consumption and are least able to hold assets that aren't cash... hell: we make laws that actively limit or even prevent poorer people from holding non-cash assets "for their own protection").

That blows my mind. I'm allowed to spend $10 in a bottle of alcohol or a packet or cigarettes, no questions asked, but I'm not allowed to spend those $10 in stocks of a tiny company unless I'm able to demonstrate that I sleep with the founders or make their lunch or run their accounting, or that I have so many millions on my name that investing $10 without doing any of the above really could not harm me.

It's not like accreditation exists to ensure poor people stay poor, framing it like that is disingenuous. Small-time investors are unlikely to be able to even semi-accurately estimate the value of a company, so they're much much more likely to be tricked into overpaying.

It isn't that it exists for that reason, it merely has that effect as a callous side effect of not really caring about the power imbalance it causes on said poorer people. "The road to hell is paved with good intentions" 100% applies to people trying to protect other people from none other than themselves.

> Doesn't that practically mean the rich get richer and the poor stay poor? If it would be net 0 everything would stay the same?

The rich aren't rich through this route, although things they do mean that bank interest rates are a guaranteed return for people who are less risk-tolerant. They're rich through one or more of: risk-taking, talent, hard work, luck, connections, etc, all of which feed into the one thing that makes them money: usefulness to other people.

Not because of this one thing, every bank offers some return on holding cash. Most are ridiculously low.

Personally I like to think of it as, the US govt guarantees a return on overnight cash based on the Federal funds rate. Banks and other people that hold cash will give you that rate minus some fee(s) for the hassle of keeping up with your cash for you. Most banks have a very hefty fee, but not all banks.

As of this writing:

The Federal Reserve will pay 2.56% for cash deposited with them.

Bank Of America pays 0.01%, for a fee of 2.55%/yr.

Ally bank pays 2.25% for their savings account for a cost of .31%/yr

If you are willing to hold cash in an ETF, ICSH will hold cash for a 0.08%/yr fee.

For the record, I'm not against Bank Of America, I have an account with them, but I don't hold much, if any, cash with them for any length of time, because I know they charge a lot for that service.

Yes, if it were not for the inherent risk that comes with it. If you put the cash in your mattress you only face the risk of losing it due to it being stolen or when it burns. You can get insurance against that it this would need to be deducted as well. So effectively you are losing money.

Now for money on your bank that pays interest it's not necessarily better. The bank can be robbed or simply go bankcrupt. And since the money there was used by the bank for various things, there's no guarantee you'll get it back. This inherent risk needs to be priced into the ROI.

So IF the government always saves banks with buyout, then yes. That's also why I believe it's not a great idea and people of such a bank should lose at least a part of their assets/savings to understand the fact that the money isn's just stored by the bank.

This is dumb. That's not an insult -- I'm not calling you dumb, but just your argument.

1) Banks are FDIC-insured, so unless the federal government goes under, my money can't be lost. If the US disappears, so does the dollar.

2) If people lose part of their money due to a policy like the one you propose, they won't "learn." You're asking ordinary people to be aware of things which are accessible to a fraction of a percent of the population. They'll assume banks are safe, and lose trust in "the system" if they're not.

3) Even so, I have no way of knowing what's going on at my bank. For all I know, the executives might be crooks embezzling money for the Italian mafia. We have organizations like the FBI, SEC, etc. since individuals can't investigate these things. I'd like to focus on my family and my job. That's why we've specialized.

The current approach for banking is better than free market. Personally, I think banking would best be nationalized, a la China. It's not an industry where efficient free markets do very well. That's true for health care and parts of real estate too. (And yes, there are other industries I would privatize much more, like education. This shouldn't be an ideological socialist versus free market argument, so much as looking at the extent to which free market assumptions apply to a given industry)

> This is dumb. That's not an insult -- I'm not calling you dumb, but just your argument.

No worries, I'm here to discuss and learn things, so happy about your reply!

> 1) Banks are FDIC-insured, so unless the federal government goes under, my money can't be lost. If the US disappears, so does the dollar.

Yes, but there is still the chance of a "haircut" or similar. At this scale, rules can be bend. But my response was a bit more independent of the country, so maybe it doesn't apply well to the US, point taken.

> 2) If people lose part of their money due to a policy like the one you propose, they won't "learn." You're asking ordinary people to be aware of things which are accessible to a fraction of a percent of the population. They'll assume banks are safe, and lose trust in "the system" if they're not.

Maybe for the first time. But if you think about it, maybe the system is how it is _because_ people trust in it (too) much.

There are a couple of options. For instance, the state can give a guarantee for only a limited amount of money (think $20k or something like that) per person and/or institute.

Second, it might very well be that banks will come up with two different kinds of accounts: 1) an account where the money is not safe and can be used by the bank for investments - but you get interest. 2) an account where the money is safe, but you don't get interest but have to pay a fee for the bank's services. The money then stays your property and the bank just keeps it for you, so even if it goes bankcrupt, no one can take the money since it's still yours.

I don't think that would be a bad idea.

> 3) Even so, I have no way of knowing what's going on at my bank. For all I know, the executives might be crooks embezzling money for the Italian mafia. We have organizations like the FBI, SEC, etc. since individuals can't investigate these things. I'd like to focus on my family and my job. That's why we've specialized.

I believe that for your health, your relationships (friends, familiy, ...) and your finances, you cannot delegate that, you must keep control yourselve. You can get people to help you, but in the end both control and responsibility are yours. That's what I think works best.

> No worries, I'm here to discuss and learn things, so happy about your reply!

Thank you! I enjoy discussions with folks like you.

> Maybe for the first time.

If we're having regular bank failures, we're going to enter "failed state" status. Can you name any nation which regular bank failures which isn't a hellhole?

People don't learn from once-in-a-lifetime events.

It's also not what I want people to learn. Systems like this ought to work well enough in a well-governed country that ordinary individuals don't need to think about it.

The US has problems, but not at the level of people worrying if their bank accounts will disappear tomorrow.

I also want sufficiently functioning police departments that people don't need to worry about how to defend themselves. There are things which ought to work. Retirement savings ought to be one of those.

> For instance, the state can give a guarantee for only a limited amount of money (think $20k or something like that) per person and/or institute.

The current limit is $250k. This seems reasonable, and potentially low. I'd set it at $1M, and include accounts like 401k and IRA accounts, so your retirement investment savings can't disappear in a poof for reasons outside of your control. If I bought stocks, I can (and should) expect their value to change, but I should be able to count on Fidelity safely making sure those are still my stocks.

> Second, it might very well be that banks will come up with two different kinds of accounts.

It might well be. 0.1% of the population will chose wisely. Like medicine, this is something you want to just work.

> I believe that for your health, your relationships (friends, familiy, ...) and your finances, you cannot delegate that, you must keep control yourselve. You can get people to help you, but in the end both control and responsibility are yours. That's what I think works best.

Why? All evidence suggests the contrary:

- People seem happiest in communal societies, where they don't pick their friends or family. We evolved in tribes.

- I'd love to live in a structure where I get healthy food and plenty of exercise as a "default." Staying healthy with companies marketing high-sugar foods, and obsolete parts of my brain pushing me to be lazy, is a constant uphill battle. I'd stop short of a mandate, but if everyone is healthy, we're all better off.

- Finance is a black hole for most people. People ought to be able to trust that if they work hard, they'll be able to afford basic food, shelter, and medicine (including in retirement). It feels like a trap to make people manage this.

If my life consisted of:

- Wake up for morning exercises. There are plenty of communal spaces for exercise. Volunteers run free dance, martial arts, yoga, etc. classes. My taxes fund the space.

- Work hard on open source, which benefits everyone, for some number of hours

- Spend time with my family

- Not worry about much of anything else, and count on systems working

I'd be pretty happy. We haven't figured out how to do that, but utopian ideals don't have everyone needing to investigate their local hospitals for corruption, banks for fraud, and mastering medicine and finance. As a nerd, I enjoy learning about those, but it shouldn't be mandatory.

> Can you name any nation which regular bank failures which isn't a hellhole?

That's a bit unfair, because there is no country (yet) where there is a system similar to what I proposed. If there were, then maybe it would be pretty normal and putting money on the bank that yields interest will just be seen and regulated as investing into stocks nowadays.

> It's also not what I want people to learn. Systems like this ought to work well enough in a well-governed country that ordinary individuals don't need to think about it.

To me it feels like you are trying to push away a responsibility that is impossible to push away. (sorry for me bad English)

What I mean is, once someone gives money to the bank and the bank _uses_ it instead of storing it (e.g. for a loan/credit) then there _is_ a risk that the money will be lost.

So if you want banks to be failsafe in the sense that it is legally guaranteed that you can never lose your money (currently that's not the case right) then banks should be fully government controlled or at least so tightly regulated that they are very very different from a regular business. I mean, banks are already highly regulated, but not nearly enough in my opinion. If the bank can't lose/go bankcrup, then it also shouldn't win, so no profit or highly regulated profit.

EDIT: I forgot to say that if the state is essentially insurance for the bank, it should charge for that service just like a normal insurance company would.

> Why? All evidence suggests the contrary: (...)

None of the points contradicts what I said.

But look: even in a communal society YOU pick your friends, no one else. And if there are two kinds of foods, one tasty, cheap and unhealthy und one so-so, kinda expensive but healthy, would YOU trust the advertisements which one to pick?

Even with a doctor: sure, it's great to have competent doctors. But it's a fact that there are better and worse doctors. So if health is important to you, YOU have to pick the right doctor. If you rely on someone else to do so, you are essentially putting your life in their hands. While anyone can decide to do that, I just don't think that it's a good idea.

The problem with your nice example life is that once things go southwards (and eventually they always do) then you can't deal with it. I prefer a slightly less optimal system that has less potential to go really bad, even if average quality of life is a bit lower.

> That's a bit unfair, because there is no country (yet) where there is a system similar to what I proposed. If there were, then maybe it would be pretty normal and putting money on the bank that yields interest will just be seen and regulated as investing into stocks nowadays.

You can do this in the USA, look up the ETF ICSH for instance :)

Yeah but that’s not the whole picture… in 1962 the ford truck was $2000 now is around 40,000 so while a new one is better you still have to earn 2x as much to get the most basic one available

When I go to ford.com and look at their basic truck, the 2023 Maverick, I see "starting at $22,195". So if a 1962 truck truly sold for $2000, the inflation seems to account for entirely the price increase. And I'm pretty sure everyone will agree a 2023 Maverick is superior to a 1962 F-100 in every conceivable aspect.

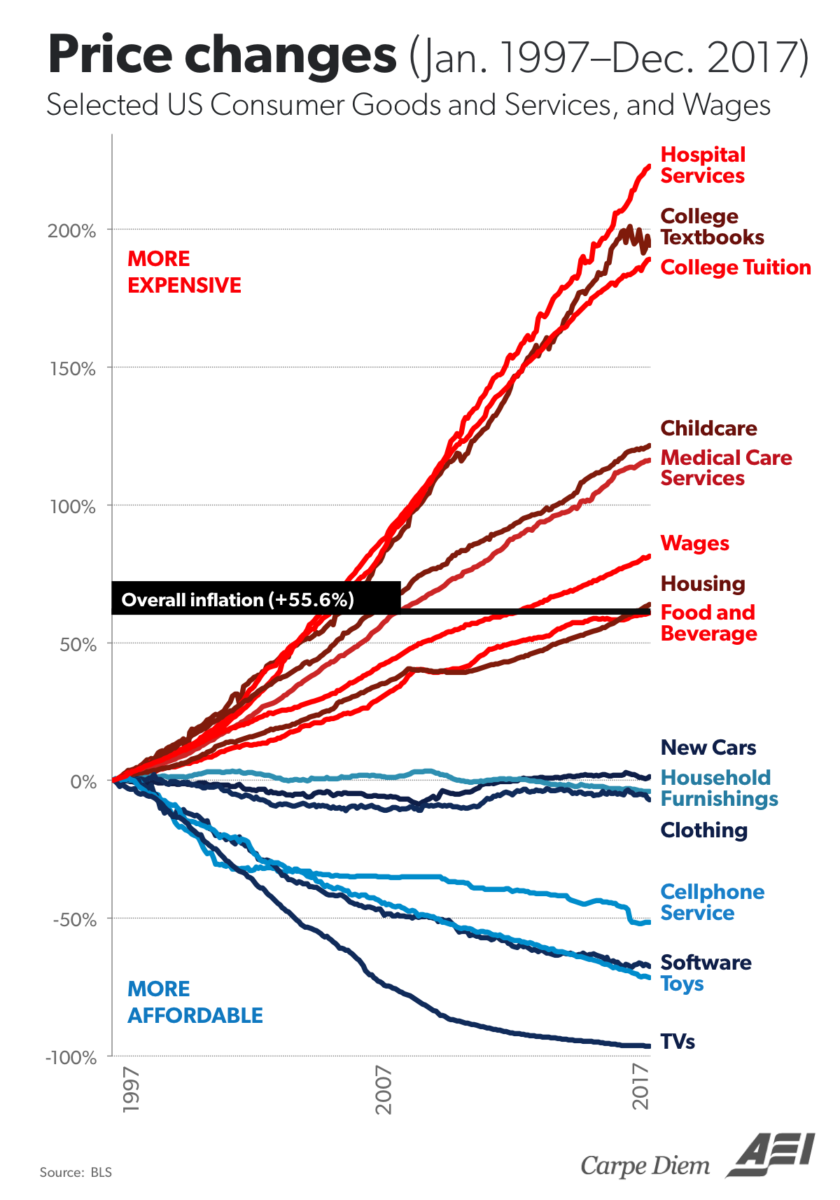

Housing and healthcare are better examples of goods or services whose prices have increased faster than CPI-U.

In the 80s when I was a kid, we owned our own house, even though my father was a small time farmer and my mother stayed home raising us. We scraped by. In today's standards, it was a life of abject poverty. I knew a guy whose father ran a steel company (self made millionaire). Their house wasn't much bigger than ours, but they had VCR, microwave, CD players and satellite TV years before we did. But the real difference was that they had a new Mercedes and we had a low-end Ford that we drove until it fell apart. Our house build cost about 4x the price of the Ford. The Merc? I don't have exact figures but I think you could have built our house at least 2.5x times before you hit the price of a new Merc. These days that's totally flipped around. For the cost of building my parents house today, you could have at least 4x new Mercs.

In the 1920s it was cheaper to retain a servant full time than to own a car. Now it's completely the other way round, and for a car a million times better. Production of goods scales; anything labour-intensive does not, especially when land supply and usage are constrained by government regulation, and cost of labo[u]r is inflated by same.

I'd be surprised if you can get a truck at anywhere near MSRP these days. Trucks aren't a great example anyways because they're seen as a luxury good in the US today, which wasn't the case in the 60s.

Check the new car market again. Buyers have radically cut back as the economic uncertainty has proceeded since summer, plus the supply chain issues continue receding into the past.

First, you can't get the old vehicle new for cheap. That option is no longer available. You do get an objectively better one, but value is fundamentally subjective.

Marginal economics bridges this gap with consumer choice, but if no choice is available then I don't think you can assume consumers are better off.

In any case, I think inflation is a backwards lens through which to examine vehicle prices. The primary mover is industrial learning curves. Inflation is downstream.

In the 20s, when domestic car sales increased annually, the auto manufacturing industry was constantly growing. Factory efficiency increased every year and prices came down every year. The model T got cheaper every year, not just better.

Part of what caused the depression was this process maturing. Auto sales peaked. Manufacturing volume stopped growing. Efficiency stopped growing with it.

This breaks many financial assumptions/instruments and results in deflation, or rather, a local quanta of deflation. Growth industries can vary a lot of long term debt/equity/promises. Shifting from one state to another is deflationary/deleveraging.

Anyway, vehicles stopped getting cheaper 100 years ago. They get better/nicer gradually. Not cheaper though, ever.

Cars don’t break down as much and last much longer. A 20 year old car nowadays can still be perfectly usable. So in effectively they did get cheaper, just buy used (at least that was the case until 2020..)

Same, also one that is 40 and one that is 60. There hasn’t really been an increase in reliability over time. The difference between manufacturers has always been the defining factor. Simply compare a new Nissan to a new Toyota and you’ll see what I mean. Project out resale value 10 years and you’ll see a dramatic drop in value for the less reliable one. It was cheaper to manufacture, used lower quality parts and engineering and the result is wildly different reliability.

The F-150 is the lowest cost full size pickup truck Ford makes. If you can't put full sheets of plywood and 2x4s in it, it's not really a pickup truck.

How Much Does the Ford F-150 Cost?

The 2022 Ford F-150 starts at $29,990, which is the lowest base price in the full-size pickup truck segment. However, that's for the three-seat Regular Cab, so if you're looking for more room, take note of the Super Cab's $34,075 base price and the SuperCrew's $37,700 MSRP.

The 2022 Maverick has an engine literally twice more powerful than the 1962 F-100 (270 vs 135 hp). With your logic, picking on one tech detail of many, I could argue the 1962 model is "not really a pickup truck" with such a puny engine of weak towing abilities !

What this shows is that Ford merely decided to trade 18 inches of pickup box space for a second row of seat, a more powerful engine, and many other higher-end specs. Today Ford could definitely make a 1962-spec'd pickup with a weak 135 hp engine at less than $20k.

The one tech detail chosen is pretty relevant to the economic (as opposed to style) use-case here.

Being able to carry a 4x8' sheet is the difference between a productive vehicle or not for a significant chunk of the contracting tradesman market.

Sure, lots of users want trucks for other reasons where a short box does fine or a second row of seat is the winning feature regardless of box space, but the logic being applied for a full size bed requirement isn't arbitrary.

I want a full bed. As a result when I looked I was doing so in the past. Came close to buying a VW flatbed with a tools compartment built in. Thing was from the 60s.

I suspect that to an extent, prices rise with the proportion of income people are willing to allocate to something. Cars will rise to the amount that matches the importance people place on them. If cars become less important due to electric bikes and Zoom, manufacturers will be able to charge less. The investment in researching car design would decrease accordingly. Same with energy sources etc.

True, but only for goods with a moat. Let's say an iPhone. I may value a fruit at 10 Euros and you may sell me a fruit at that price, but if someone else can produce them for 2 Euros they will perhaps sell them for 5 Euros and make a good profit. So the price will be 5 or even less.

I’d prefer a brand new 62 f-150 to a 2023 maverick.

But yeah housing is a better example. We really fucked that one up didn’t we?

Healthcare is hard because we have so many better technologies, but worse outcomes so the price increase is arguably not worth it. Maybe this one is like the truck. Lotta new technology, at the end of the day not better.

And most people rarely need a pickup truck for its specifically design utility. They likely just want a safer car which is essentially an arms race at that point. I think less pickup trucks on the road would be a good thing considering how the majority of people drive.

Are modern pickup trucks objectively safer than modern cars, or is it more about the perception of driving something that feels it's half way to being an armoured vehicle?

In Europe almost no-one drives around in a truck. Even the tradespeople (carpenters, plumbers, roofers, gardeners, heating installers, you name it) all drive light vans, not trucks.

> In a collision with a significantly lighter/smaller car? Usually

Can you give a source for that?

I'm struggling to find anything up to date which isn't blatantly biased, so here's something (old!) from Berkeley Lab:

'Those who think that driving big is driving safe, or that lightweight, fuel-efficient vehicles are inherently more dangerous than their heavyweight counterparts, need to think again. A researcher with Lawrence Berkeley National Lab (Berkeley Lab) has teamed with a researcher from the University of Michigan in a unique risk analysis study which shows that, contrary to conventional wisdom, vehicle quality is a much more important safety factor than weight for the drivers of vehicles involved in a crash.

"Most cars are safer than the average sports utility vehicle [SUV], while pickup trucks are much less safe than all other types. Minivans and import luxury cars have the safest records," states the report, "An Analysis of Traffic Deaths by Vehicle Type and Model," which was prepared by Tom Wenzel, an energy analyst with Berkeley Lab's Environmental Energy Technologies Division, and Marc Ross, a professor in Michigan's Applied Physics Department.'

You can't just pick one single item and consider it 'representative' of inflation. [1] Some things cost more than they used to, some less. Cars happen to have tracked very well.

That doesn't match my experiences; IME cars do last longer now.

I have owned and spent substantial time driving a 1978 Buick Regal and a 1968 Westphalia VW van.

I don't think that you're gonna see 200K miles out of either of those vehicles. The Buick had about 120K on it and was clearly on its last legs. It's likely been scrapped. The VW only runs because I sold it to a mechanical engineer who wanted to have a project to work on with his children, and it's now a "vintage" toy instead of my daily driver.

I am at about 180K on my 2014 Tacoma and I expect to get at least another 120k out of it before I sell it.

random anecdote: 2004 chrysler Sebring - nothing special, hit 180k before I had some 'unknown' engine problem. Mechanic spent a couple hours trying some stuff, and something worked, and I got another 60k miles out of it before it was time to let it go. That was over a 14 year period. If I was mechanically inclined, I probably could have done a little bit more on my own re: preventative/etc, to get a bit more out of it. Or... had I sunk another $2k in (estimate) to fix a bunch of stuff, who knows? I might have got another few years. But I went with something smaller, newer, better mpg, and probably overall better safety (12 years newer).

People are extremely overestimating how cars last decades ago. Barring other things, corrosion protection was nonexistent, few year old cars were rusting away.

I had no idea that kids in 1962 were spending $100 on one piece of licorice. Kinda puts the “millennials and their avocado toast” thing in perspective, huh?

This is a nice demonstration of the variability of inflation and how under-trend we have been for many years. There was a strong push from some monetary policy people to move toward a longer term, average inflation targeting that would make the Fed have symmetric reaction functions to upside and downside inflation while attempting to keep a longer term average as the goal.

One interesting explanation for high inflation during the 1970s to early 1980s was that the monetary system and supply of real assets had to adjust to a massive influx of working age adults (babyboomers). A second wave from that population event started to enter the workforce over the last ten years. It might be interesting to normalize the data here against the size of the workforce.

My partial theory is oil production grew exponentially up till a bit after 1970. And before that the US had outstripped domestic supply and started having to import oil.

And you are right boomers household formation increased demand for stuff.

The most dangerous thing that can happen to an advanced economy is credit markets grinding to a halt. It was the panic of 1907 that created the federal reserve in the first place.

Over the ensuing decades there was a very awkward path to eventually figuring out that at the moments where a complete halt to credit markets looks imminent, the fed should step in and release the jam. What we’ve learned is that just the knowledge of the fed being able to just print and buy any debt and that they would do so caused major crises to be avoided (2008 and 2020).

The problem recently has been that this fed is simply incompetent. They do not form their own opinions and simply follow what the prevailing narrative dictates. If it’s consensus that rates should not be lifted, they just coast through those meetings towing the same line and continuing to buy bonds.

Then one day the narrative shifts and concern starts to grow over fed policy. So the fed suddenly reverses course and announces sudden rate hikes. When it turns out that cpi moves slower than the fed hoped, the pressure to intervene grows.

Now the consensus is that the fed should be making multiple 75-100 bps hikes so that’s what they do.

The question now is will the narrative shift fast enough for them to not end up going too far the other way.

I sincerely hope the next fed chair is someone who understands the relationship between credit markets and the economy and the need at times for the fed to be the lender of last resort, but also understands that the fed should be an independent entity capable of forming its own policy and having the courage to ignore what market pundits say should be done. The Fed’s mandate is not to make Wall Street happy.

We want to avoid structural damage: Lost jobs, bankrupt businesses, lost mortgages, and so on. Structural damage leads to loss of real productivity, and real harm to people's lives. The only way I knew to get through COVID shutdowns was to devalue currency by about as much as we've done.

I didn't mind the short-term money printing, and I expected inflation to result. The inflation is painful, but the alternative is much more painful. My income buys less than it did two years ago, but I'm thankful I have a job. I was even more thankful when jobs were easy to come by. If my employer went under or I lost my job, I'd be profoundly unhappy.

The right approach now would be to accept a dollar is worth less than it was before, and to give an honest estimate of how much less.

Aggressively trying to control inflation by raising interest rates is a lost cause, and will do a lot of real harm. The outcome here seems to be that rather than mitigating the harm of COVID shutdowns, we've delayed them, and did a lot more harm along the way.

"We want to avoid structural damage: Lost jobs, bankrupt businesses, lost mortgages, and so on."

I disagree - I think what we need is a constant, low, background level of structural damage - which includes lost jobs and especially bankrupt businesses.

I grow increasingly fond of the forest fire / controlled burns analogy:

We have come to realize that preventing, or extinguishing, every wildland fire causes a dangerous level of fuels to slowly build up, eventually erupting in an unstoppable conflagration that destroys much more than the sum of the fuel overload.

Preventing recessions and keeping business firms afloat that would otherwise fail without easy loan rollover - that's the financial equivalent of refusing to maintain fuel loads with controlled burns.

Eventually the dead fuels (zombie business firms) will overwhelm all firefighting efforts (QE ? Negative interest rates ?) and will take down a much larger portion of the economy than otherwise would have failed along the way ...

> We want to avoid structural damage: Lost jobs, bankrupt businesses

Completely incorrect. If the jobs and businesses in question existed only due to speculative excess, they shouldn't exist. Easy money generates what David Graeber would call "Bullshit Jobs", that contribute anywhere from zero to negative real value production.

We want these businesses liquidated and the employees out on the street, to pursue work that actually contributes to society.

The trick is to somehow limit the collateral damage to businesses that do produce real value. I don't think that's a problem that's been solved.

Spoken very fairly. For a central banker, it's either high inflation or high unemployment. Strangely enough, they prefer the latter. Inflation affects everybody mildly, a recession affects the unlucky few that lose their jobs very badly

Elsewhere in this subthread I pointed out that California is not printing money; it's spending surplus from 2021. California cannot print money bc we use US dollars and not CA dollars.

But I think a more interesting aspect of this is the cynical way language around the same idea has changed. The Franchise Tax Board is calling them a "tax refund", though your "refund" is based on your income being low, rather than your tax bill having been high. But the press has certainly been cooperative in calling them "inflation relief" recently, though the program was planned before inflation rose to the top of so many people's list of concerns. Politically, Newsome wants as much credit as possible for handing back a windfall of taxpayer money that came in mostly because of economic conditions he did not create and taxes that he did not introduce.

In this case they're using debt, because while they may have had a surplus in a single calendar year, they're still over $150bn in debt. So it isn't spending surplus, because they're massively underwater and a "profit" is meaningless.

California doesn't print money, the Federal Reserve does. California is required to balance its budget by law, like every state but Vermont. Nearly every state has more money than normal right now (some of it from high tax revenues due to nearly full employment, some due to federal stimulus), so they're finding ways of getting rid of the money. This is a second order effect from the much too large stimulus in 2020/2021.

The only reason the states are afloat right now is because the federal government gave them hundreds of billions in printed money. So, yeah, it’s printed all the same.

1. Federal reserve makes several trillions in new money and lends it to the US Government.

2. The US Government passes “infrastructure” and “Covid relief” bills that shower billions on states and cities.

If not for this flow of printed money, most of the states would be cutting budgets since 2020.

You know, if there is a world where money isn't printed but people refer to it as printing, then maybe at some point the government will do exactly that because people don't seem to be concerned about the rate at which money is being spent nor do they care if the government does it or not, they just want to complain.

Thank you for posting this! Suburban infrastructure essentially steals from the economically productive areas and gives to the wealthy and unproductive regions

CA HSR is moving ahead. Major infrastructure projects are more difficult and expensive in the US because we have far stronger property rights than China or European nations.

... minus the "HS" part. Last I checked it was on the politically brokered "non-I-5" corridor (a silly, absurd route) and had a proposed SF->LA trip time of over 2.5 hours.

This is a "high speed" train, circa 1975. Current technology, as demonstrated by running trains elsewhere in the world, would make that route in under 2 hours.

Why is stabilizing human beings economic anxiety not useful?

What theory of science dictates infrastructure is the best place to spend it? If the answer is none, it’s a purely social policy and you’re spewing politically correct memory. That infra spend is not an immutable law of reality means there are options other than “poison the sky with expansive vanity projects.”

Even then, there’s plenty of money for both, and human agency available for both. We can stop pretending money is what drives human invention and discovery. It’s politically correct spoken tradition since it’s not an immutable law; how we feel about other economic choices is a range of possibilities, not just the ones we have been raised to speak of

The excess tax revenues was also caused by overly inflated IPOs and more than normal capital gains. At least in CA, if the surplus is large enough the government is legally required to give the money back if not spent.

Gavin Newsom in this case is acting like Robinhood. Taking from the rich and giving to the less well off.

He's taking from the children of the recipients, considering California's current debt load. When you're underwater, a "profit" doesn't mean you're suddenly flush with cash. It's still debt-funded frivolity, which will paid by children.

That's over half the usual budget for California, so no it's not "peanuts". The ability to service debt is a function of the government's resources, not the entire economy. As pointed out, the year was anomalous for California, who usually runs a deficit of over $50,000,000,000.

Seems like this is a case of a compulsive indebted gambler patting himself on the back for a good streak at the tables.

California's surplus came from temporarily increased CGT receipts. That trend will be reversed this year considering the markets, and they'll be back to bleeding 10 figures.

Government debt is not like personal debt. Governments debt is structured and has fixed predictable rates (bonds etc). There's no incentive to pay down debt because the debt holders want long term structured repayment.

The only time government debt is bad is when the government can't make the payments.

A charitable interpretation of the comment above would assume that the taxes being collected are primarily the result of printed money, or at least that the fed's printed money forms a large portion of these revenues which are again being redistributed. It's actually quite sneaky. Print money to stimulate the economy and then tax it back out to redistribute. You just printed the poor into 'wealth', but did it in an incredibly roundabout way that saves all the politicians face.

Yeah in the grand scheme of things, this doesn’t impact inflation all that much, but it does help the people that need it most. Just like increasing the minimum wage to keep up with inflation does.

Over the past year businesses have increased their prices all over the board, you can’t then just simply say “but inflation!!” when you want to help the people with some amount of compensation for this.

If you take it just one step further, the people "that need it most" really only need it in order to instantly donate it to the megacorps with pricing power at ever-increasing prices. The handouts help only in that instant and at the very next clock cycle that money is now in the hands of the megacorps. Printing money and handouts only help the top of the top in the pricing power hierarchy. If you want to actually help people you'd be doing taxes on excess. Everything else ends up in gigantic accumulation of wealth at the top in just a few steps down the game.

From that perspective, anything always ends up in the top of the top of megacorps, and I find it not a very compelling argument to not help people just because they’re at the mercy of megacorps.

You want to tax these megacorps additionally yes, especially if they’re profiting from the current situation. But at the same time, it’s also important to redestribute that wealth towards those who have the biggest problems right now.

With handouts, you only redistribute the wealth for an instant and you need to keep printing to sustain it. On top of that, the stability of this system becomes dependent on active approach of handing out money (i.e. tight dependency on central government).

And I am not saying not to help the poor people. I am saying printing money doesn't help poor people, it helps the rich. If you want to help poor people like I said you can tax the excess, or you can provide a specific minimal food/energy/shelter. But again, handing out money for free only helps the top of top.

As a side note, you know a lot of the poorest people in EM and frontier markets save money in USD either to escape their own inflating currency or as a dollar peg in their country. These people are poor and suffer the inflation in global markets, but they do not benefit from the US handouts. They can never outbid a money printer. And that's in fact the likely cause of the riots across the world in countries that don't have swap lines with the Fed.

But we used taxpayer money to first inject trillions into the top of the economy. And then when the inevitable happens, we can’t just throw our arms in the air “because inflation!” — that’s a great way to make sure that the bottom of the economy will suffer tremendously due to all this.

Because their income hasn’t increased nearly as much as the amount of inflation that occurred.

Then try getting paid outside of civilized society. Unemployment will never be zero. An economy can't be 100% efficient. Taking care of those who cannot find work due to an imperfect system is a part of a civilized society.

Also, it would be inefficient to have an unemployment rate near 0. People in a good job market need to leave bad jobs, and sometimes that means that they are unemployed.

That doesn't make sense though. You can't create energy by printing money. You just redistribute the value of your money. Maybe that's good - not clear to me why it's better to use inflation, which risks destabilizing the currency and punishes people who saved money, rather than straightforward taxes.

But in the Californian case, it's not printing money. The state government doesn't have the ability to make US dollars. The state must balance its budget, and cannot rely on debt the way the federal government does. The inflation checks are only possible because of a giant, historic budget surplus from 2021. Had inflation not gotten this bad, the checks would have still gone out in some other form (earlier in 2022 we were talking about it as a "tax rebate").

Though this action is redistributive, it is explicitly not about printing money. It is about spending excess tax dollars. You may have opinions about taxes in the state, and you may have opinions about redistribution, but overall if the state temporarily has a surplus (ie it shouldn't put this money towards increasing long running programs that will become a burden in future years), shouldn't it give that money back to the citizens in some form?

Complaining about printing money is like complaining about the internal combustion engine in an electric vehicle. This is especially annoying when what people are really asking for is a speed limit. But since everyone keeps talking about the wrong thing nothing will get done just like how an ICE mechanic isn't going to fix your EV.

I never said that it was inflationary in the California case. I don't think it is. As to whether or not the state should send checks to everyone - I don't really know anything about it and so don't have a firm opinion. My intuition is that individuals will likely spend the money better than the state would have, so that's good, and it's probably an indication that taxes are too high if the state has a big surplus.

California doesn't distinguish between capital gains and other income, and both are taxed on a progressive bracket system. In years where lots of rich people realize gains, the state has more income. Plus wage growth.

But Keynes advocated that governments should have surpluses in good times and spend more in bad ones. Normally because the state isn't able to carry a continuing large surplus, this isn't possible; it has to cut in lean years and give rebates otherwise. It's only in this short period of reversal in consecutive years that we can approach that policy. I'm guessing the same checks would have done more good if they could have waited until 2023 or later.

If you create money and give it to people, they spend it. That creates additional taxation. That spending is earned, which is taxed. The earnings are then spent, which is taxed, and so on. Like a stone skipping across a pond.

Do the fairly simple geometric series from that and you'll discover that all money creation generates additional taxation that extinguishes it - to the penny. All that changes with the tax rate is the number of hops before the money impulse disappears.

What you have to do to balance the system is remove some hops elsewhere. That's what threats about interest rate rises are supposed to do. Money then isn't created by loans, or the transaction hops from those loan creation events are fewer.

That reduction is what we call 'saving' and tends to show up in aggregate as a government deficit. The bigger the deficit, the more saving there was and the fewer transaction hops in the economy.

Saving is little more than voluntary taxation. The current approach is to go down the voluntary route rather than the compulsory one - largely because the population won't sanction any further taxes.

If the money used to purchase energy causes a large rise in the government deficit (or a significant reduction in the loan growth rate) then that will 'pay' for it without causing inflation.

Yes but the energy crisis isn't evenly distributed across the world. NA, for example, is still doing relatively well. While Europe is being hit relatively hard by the shortage and will likely have to import from more expensive sources than previous years to make it through the winter.

How would European governments printing more of their own currencies to give handouts to their citizens, resulting in inflation, resulting in their currencies becoming weaker, help buying energy from NA?

The energy has already been paid for since European countries have been overcharged for gas during most of 2022 in order to fill their storage to at least 80% before winter. Energy bills are usually paid by the quarter or by the year—not daily—so in some cases the worst part has yet to reach consumers.

Furthermore, the way the European electricity market works[1], other energy sources are also bid up when the price of gas increases iff this gas is needed to ensure supply in a given hour of the day. So we have been overcharged both directly (gas), mostly indirectly (electricity) and completely indirectly (goods inflation) throughout all of 2022. This is seriously hollowing out the budgets of some European families.

I don't agree that blanket handouts are the solution, but some kind of compensation is needed to those most exposed, otherwise they will sink into poverty.

Not everyone gets the same amount of money, so that poorer people benefit from the scheme while richer people are more affected by the increased inflation.

Rich people are less affected by inflation because they have access to investment opportunities that aren't as affected - for example, I'm sure German billionaires have money in American hedge funds. The middle class are most negatively affected by the tax of inflation because they have enough money that having the value of it reduced by inflation is meaningful, but they don't have sophisticated investment instruments to hedge against inflation.

This takes us back to what I wrote originally - why is inflation the way to do this as opposed to just tax and spend? That is, why not create a specific tax and implement that and use the proceeds to pay for poor people's energy? Money printing is just a dishonest way to sneak a tax in on people who might not recognize it as a tax.

The levers don't do exactly the same things; devaluing currency helps exports, for example.

There's also the political cost. I'm in favour of democracy in the ideal case, but obstructionism looks like a concern in some countries, people buy into lying spin and vote against their own interests, bills have their own cadence, and lawmakers are not always intellectual powerhouses. Case in point: the BoE reacted within hours to reduce the damage done by Liz Truss

>That doesn't make sense though. You can't create energy by printing money.

Think again. You can't create energy by cutting taxes either. The tax cut can only be spent on energy, exacerbating the problem by making wasting energy much cheaper.

A check on the other hand discourages people to buy expensive energy because they could be spending the subsidy on something else that isn't energy constrained.

The problem is that the world is at neoliberal capitalism's end, as predicted by Marx. Basically, in capitalism, you pay for continuing investment (of capital owners) with giving them more property, which is something that cannot continue indefinitely. That internally increases social inequality, and the money will eventually accumulate at the top (in the form of asset price rises).

Capitalism's own solution so far was to create more available properties - more individual debt such as credit cards and mortgages, privatize public goods like health and education, more destruction of ecosystems, selling attention and disrupting work, and the latest fad, cryptocurrencies. But these are only temporary solutions, they do not address the core problem of increasing social inequality.

Likewise, printing money and giving them to the poor (while half of it goes directly to the top, because the decision-makers are only human) is a stopgap solution in the system where most money quickly end up accumulated at the top. It's a desperate attempt by governments to maintain social order.

In the middle of 20th century, the capitalism's tendency to create disparity was somewhat resolved in Keynesian approach, where state "investments" (based on taxation) were basically redistribution of the money back to the bottom, so that the process of accumulation could continue slower and indefinitely. That was eventually abandoned, for ideological reasons (people shouldn't get "free money", and the "private property" is sacrosanct).

However, it is the only known solution. The proper taxation of the rich (and property) is badly needed to long-term stabilize the capitalist system.

One could make an analogy with any other competition. When another competition starts, winners (of the old competition) are usually given the same place at the start as everybody else. This is because without this rule, the competition would quickly demotivate everybody. But this is happening under neoliberalism, and threatens to eventually halt the positives of the capitalist competition.

> The problem is that the world is at neoliberal capitalism's end, as predicted by Marx

Well. Its capitalism's end. Neoliberalism is just an attempt to return to actual capitalism that existed back at the end of the 19th century. Before those pesky regulations, antitrust laws, all those workers' movements and rights for the plebs...

Given that California can't print money, why do you think those checks are "printing money"?

And no, it's not a "sneaky backdoor". It's the government doing what it should do, tighten financial inequality gaps. And preventing unnecessary suffering. We're still a society, we occasionally take care of the weaker people amongst us. (Frankly, not often enough)

And "without real oversight" is... you're aware this is going through the normal process of fund allocation, is reported widely in the press, and is part of the data that voters can take into account next round, no? It has just as much oversight as any other government spending. (Arguably more than some federal programs)

I get that fiscally conservative folks might disagree with this, and we can certainly debate merits. But "printing money" and "without oversight" are empty slogans without basis in fact.

Nowadays everyone prints money, didn't you read internet comments. If I loan you five dollars I have printed five dollars because the contract we signed counts as a certificate of deposit in the minds of these people.

Yes, people are ignoring the second-order effects. Just because California can’t directly print money doesn’t mean they aren’t contributing to the macroeconomic factors leading to the Fed feeling the need to print more money.

Right. One way to combat inflation is to save money. The fed encourages this by increasing the interest rate. If california truly wanted to reduce inflation, it would simply retain those $1000 checks. Taking money out of supply reduces inflation.

California doesn't want to reduce inflation. (It would be of at least questionable legality, too. Because monetary policy lies with the federal government - Article 1, Section 8)

What California does want to do is ensure poorer people aren't bearing the load disproportionately.

Also, while we can certainly argue if this is the best use of those funds, a quick reminder that the size of the US money supply is almost 22 trillion. We're about $6T above 2019 levels. California retaining $10B is not going to have any measurable impact on inflation.

Sounds like a decent recipe for boosting the economy, assuming the supply side capacity is available: injects a bunch of demand, but at the same time, precisely by being a one-time measure, discourages price hikes.

We have printed so much money, the only solution is to... print more?

Yes. Once you start printing money to fix problems, you fall into the pit of always needing to print more. See Zimbabwe’s $100 trillion dollar bill. I have one, it makes a great placemat.

yes. even though technically california doesnt 'print money'. people are more important than economy. the 'redistribution' is happening to help the most vulnerable and that's exactly what surpluses should be used for..seems like a good use of money to me.

I hate it when people make it seem like the economy and the people are two different things.

The economy is the aggregate capability of a society to provide goods and services to people, if the economy collapses the goods and services that are being provided cease to be as well and people are worse off.

Short sighted statements like "people are more important than the economy" is a feel good virtue signaling that is indicative of an inability to think clearly about the consequences of actions and a substitution of emotional reasoning over rational thought.

I wasn’t virtue signalling. Over supply of money will make inflation worse, but constriction would bring down spending.

A labourer making daily wages and supplemented by govt dollars will spend all of it. A millionaire with a few millions in the bank is not going to spend any of it. Especially during an overheated inflationary period. It’s better spent to the most vulnerable to pay for their food, gas and utilities.

This is exactly what needs to be done to keep spending going. It’s spending from a healthy and happy middle class that keeps the economy going. Can’t freeze them out. Not implementing measures like this would collapse the economy.

An economy with hopeless disenfranchised hungry poor majority is exactly the first ingredient in the recipe for revolts and revolutions.

Also..it’s heartless to not share a surplus to people who are suffering. We are a rich country. No one died because someone else got a little extra money to pay their electricity bill or gas.

But you just explained why this causes more inflation. In your words, it was money in the banks of wealthy people, meaning not being spent. Money that isn’t spent doesn’t cause inflation because it’s not competing for goods and services.

By redistributing to poor people, that previously stationary money is now being used to compete for goods, since poor people generally spend all of their money. So more money is now chasing after the same goods, prices have to go up.

It might make people feel good in the short term, but continuing inflation also hurts the poor, and could potentially widen wealth gaps even further since the wealthy are mostly invested in assets which can keep up with inflation, but poor people’s salaries do not keep up very well.

Short term looks like a good move, but it just kicks the can and continues widening the divide of rich and poor

Non wealthy people and poor people spend on necessities. You want the money to be spent on commodity goods and generally traded goods like grain, cotton, utilities etc.

We need healthy enough money supply and sufficient money supply in circulation to keep the economy alive. If anything, this isn’t ‘charity’…it is to ensure minimum money supply to keep the economy healthy and prevent it from collapsing. But not too much to cause inflation. To deal with this, interest rates will go up.

It is more like electrolytes needed to keep the economy upright. It is not a lavish meal at a Michelin starred restaurant.

Also helpful to understand Phillips Curve and relationship between unemployment and inflation.

The govt is trying to bring down inflation to cool the economy after all the excess money supply during pandemic. That was necessary too.

So expect unemployment rates to rise in the short term. This money will help poor people and those looking at unemployment in the coming short term to survive. This is necessary. We still want them to be able to buy food and pay for gas and electricity as the correction goes underway.

Distributing more money is almost certainly unproductive.

During Covid large checks were mailed out. Reddit was full of 'casual investors' throwing money at meme stocks that explained it was 'covid money' and thus didn't matter much to them.

Student loan debt forgiveness is the latest madness.

The end result? Those with the least money (the poor, and those on fixed incomes) are totally hosed. If you can't afford rent at $800, you surely can't afford it at $1400. More handouts only make the problem worse.

The Fed's response (raising interest rates) will make cars and houses out of reach for many.

Vote for politicians of any party who pledge fiscal responsibility. As a litmus test, judge their reactions to government handouts.

> The end result? Those with the least money (the poor, and those on fixed incomes) are totally hosed. If you can't afford rent at $800, you surely can't afford it at $1400. More handouts only make the problem worse.

That's absurd; while a one-off is nowhere near as good as a basic income, a flat "handout" benefits the poor for obvious reasons (at the expense of the rich; there's no free lunch).

> The Fed's response (raising interest rates) will make cars and houses out of reach for many.

Buying cars and houses with money you don't have and hoping you can make up for it in the future is something we never should've normalised. Someone preaching "fiscal responsibility" should see this as a good thing.

How do you expect fiscal responsibility in an economic system where money both embodies purchasing power which is a stock and liquidity which is a flow? Liquidity is a costly service provided by the public, every open shop and business provides liquidity and operating a business even with no customers costs money. This means anyone holding onto money can force others to spend money on providing expensive liquidity which completely eradicates the concept of fiscal responsibility because the holders of money aren't responsible for paying for the liquidity they benefit from.

> But if the main driver of inflation is the demand side, or inflation expectations, history indicates that a painful recession could be the only way to curb inflation.

That's certainly the expected path forward, at least in the circles I associate with.

"When the tide goes out, you find out who's swimming naked" seems a reasonable guess as to what's going to happen. Both at larger bank/investment firm scale and at the individual level.

At an individual level, just how much slack and flexibility do you have in your spending, your finances, your general way of living? If you're a high earner (there are certainly plenty here that would qualify), are you spending that on lots of monthly payments of assorted luxury and stretch items (house, cars, all the other crap you can get loans for)? You're probably going to be in a world of hurt - there's no income so high you can't outspend it, and it's really hard to adjust those payments when the value of money goes down and you need more for the living expenses. Also, those payments don't go away if your job is eliminated.

If you're comfortably pulled back, with either a high savings rate or a high "optional spending" rate, then you should be in far better shape to adapt - and I'll suggest that using some of those resources to help others around you would be useful. Even just coordinating bulk buys of food and other resources is helpful. But the key here is that this allows for flexibility. It's good to be rich, and all that - so don't be stupid about it.

I think, collectively, we're in for a world of hurt. Inflation is high, and energy costs seem to be staggering back up. Europe is going to be a frozen wasteland this winter if it's anything but a warm winter, and the energy costs are already eating businesses alive out there. That's before you get to a possibility this winter, in which money doesn't help, because there's simply no energy to deliver. If the natural gas pipeline to your place are empty, welp. Doesn't help to be able to afford the energy when there's none to buy.

That does imply that you might consider some backup energy solutions for the winter. I'm a fan of kerosene lately. Less annoying to use than propane, and stores almost as well.

The last couple years have broken a lot of things. And we're only just beginning to learn how much is broken, how badly.

I went into college during the dotcom bust. Everyone told me I would be making peanuts. I'm pretty happy where I am.

I've lived my life trying to minimize the financial downsides. I want money for security, not to live the high life. I like my job, and don't feel the need to retire early - I would love to do it until I'm 6 feet under. I make a decent enough income, although not the level of many here. I bought a modest house (700k - hey, it's California) compared to what lenders wanted to lend me (1.3mil).

We could afford our expenses on two minimum wage jobs if need be. And that's with 3 kids.

> We could afford our expenses on two minimum wage jobs if need be. And that's with 3 kids.

Let's assume a $15 minimum wage. The housing one can afford on two such wages is $1,560/mo. On a $700k home, assuming 20% down, to repay the principal alone is $1,556/mo. A mortgage calculator says $3,800/mo once you have interest in there — or 73% of your gross income. And that ignores insurance & taxes. And those 3 kids.

I imagine that the OP probably has savings to fall back on (since they stress financial security), and more equity in the home than just the downpayment— not to mention that if they bought it not so recently (5-10 years back), the home value appreciation has likely been insane to still come out well ahead in even an 2008-esque crash, plus they could have refinanced at 2% fixed 30year rates in 2020-2021 drastically lowing their monthly payments even further, depending on how much equity they had.

Also, California just passed a law requiring minimum wage be $22 in some industries/companies of a certain size (and the next step will likely be rolling that out to all industries and companies, as they did with the $15 minimum wage between 2016-2020)

I experienced the same and I’ve probably enjoyed similar extremely cushy tech career experiences that also aren’t that relevant to a macro discussion but it’s nice to hear individual anecdotes

On the other hand, you've locked in presumably low rates for your debt (close to 0% hasn't been uncommon for years now) and purchased items at pre-inflation levels! So maybe you can parlay some of that leverage off with minimal losses and enjoy the free rate arbitrage for a bit.

Perhaps. I'm pretty well opposed to debt, as I've seen how it can bite people over the years, so I simply don't play those games. I'm far more likely to buy something used and pay a lot less anyway, or, ideally, something with a couple problems that I know how to fix for even less, and then fix it and use it.

The problem I have with debt is that you then have to be able to service it. There are plenty of folks in the FIRE forums who go back and forth on the topic - "To pay off your mortgage or not?" is a holy wars topic. The argument for not paying it off (and arguably taking more on) is that your investments in the market will outperform your cost of the loan, so it's free money. And it works well, for at least some time - but the FIRE movement is largely a post-2008 movement, when all the money sloshing around meant investments go up. Regardless of anything else, investments go up, so put money in them, and while few people suggested going strongly leveraged, the sentiment certainly lurked around the edges.

We'll see how that holds up if the market is cratering around the time one is unemployed. Meanwhile, "Don't have debt, have savings, and live well below your means" has been tested through an awful lot more years of human history than "Put it all in index funds."

I'm certain I've "left money on the table" with my approach, but I also keep my downside risks limited, and should I have reason to really clamp down monthly expenses, I can do so very well.

Where are you at? I ask because I have 2 mortgages and a car loan in the US and 2 are fixed rate for the entire lifetime of the loan and 1 I have 10 years until the ARM starts applying so I'm laughing all the way to the bank.

90% of US mortgages are fixed for the entire loan.

I'm in the US. I certainly could do something like that. I just won't.

I hope it works for you. That's a level of debt-based risk that neither myself nor my wife have any interest in. There have been a lot of people throughout history who thought similar arrangements were "sure things," and they were, up until they weren't and it all came down around their ankles.

We live in a very modest (manufactured, gasp!) home for our income, our "new" car is a decade old, with other vehicles ranging far older (the tractor is about 80), but still maintained in perfectly good condition and they all do exactly what we ask of them. Mostly. One of the Urals got demanding lately.

It's low stress and high slack/flexibility. Those seem useful to us.

> Concern over US natural gas supply is not warranted. At all.

How'd that work for Texas a couple winters ago? Or a decade ago? Supply is more than just what's in the ground - it's the entire infrastructure related to delivering it to the various loads, and we've demonstrated at various points that it's not in as good of shape as people like to assume.

Also, someone is literally blowing up pipelines over in Europe. Don't think US infrastructure is better guarded.

If you don't think it's an issue, great. Hopefully you're right. If you're wrong, hopefully the outages are short lived. Because otherwise people die.

Texas didn't suffer a gas shortage? There was a weather-caused generation capacity crisis, which is a rather different resource. Is that what you're thinking about?

Cold places have pretty robust gas infrastructure, but cannot grow it because of the green people with gas heat who want all new installs to be heat pumps.

2/3 of my debt payments are a sure thing as they are fixed and inflation is also a sure thing as deflation is catastrophic so governments won't allow it and deflation is trivially easy to fix with helicopter money.

The only thing that isn't a sure thing are wages but they have over the long term gone up [0] and when they do go down it is usually only for a few years.

The last one is a risk but I think it is well worth the risk.

> It doesn’t make sense to not buy the best house you can afford.

I heard that a lot in the 2006-2007 era. And plenty of people lost that "best home they could afford" back then. Fortunately, I couldn't afford a four-figure car, much less a house - though some other grad students seemed able to convince someone to offer them loans. No idea how all those worked out, I do hope some of them were able to keep the houses.

I know quite a few people who are able to afford their houses, but wish they'd purchased smaller. A larger house, all other things being equal, will cost more to heat and cool, take more time to clean and maintain, and will generally have far higher carrying costs. You can mitigate some of them, but they're quite a bit more expensive than something smaller, simpler, and cheaper to maintain.

I don't own a house as an investment. I own it as a place to live, with some land to do things outside. And at this point, our "minimum monthly spend" to keep the house climate controlled and lit is pretty darn low. Again, I recognize it's not a particularly popular point of view, especially in the tech circles, but I find "buying a big house as an investment when you don't need it" to be entirely absurd.

I wasn’t saying “you do you” sarcastically. You ultimately decide what you can afford.

Being conservative debt is a valid strategy, but has risks. Buying the house you need at 25 may not be the optimal strategy if you’re going to be there when you’re 35. Bedrooms and school districts may matter more.

In my own case, my wife and I decided that we would send our kids to private schools and wanted to maximize our family time. So we bought a house in an urban area that was perfect for our goals, had a 10 minute commute and much less expensive than a suburban house of similar nature. We borrowed, but not excessively.

Financially, it’s not a high rate of return (probably about 3% annually). My same house in a town with a good school district would have generated a 10% return. But for me, liberating 150 hours of commuting time and not having a big mortgage was valued higher.

Buying a bigger house just allows you to park more of your net worth in real estate. As a diversification it makes sense. But also as you make more money the payment becomes less and less of your monthly income.