I mean, just look at last year, when the S&P 500 index plunged over 30%, then proceeded to nearly double from then until now, in the midst of a global pandemic that froze big chunks of the world economy. Stock market returns make no sense.

It starts to when you ask yourself: Where else are people meant to store money? Since interest rates and bond rates were at historical lows. So you have people who are looking at 10% YOY returns on one hand and 0.2%/2% on the other and making the rational decision.

Does this make stocks overinflated? Yes. Is it going to suddenly pop? Unlikely, since the conditions that caused it won't suddenly change (e.g. certain bonds have ticked up 1%~ but taken months).

Money isn't stored in other assets. It's transferred from the buyer of an asset to the seller. It doesn't cease to exist simply because you traded it for stocks (or gold or anything else). Now the seller has to deal with the consequences of holding the money you previously held. A rational trader factors in the costs of money when they price assets, therefore one doesn't avoid those costs by trading money for other assets.

Right, and so the seller then has to put that money back in the market in some other asset at marginally higher prices, lest they lose money to inflation holding it in cash (or fixed-denomination assets).

This is the natural consequence of negative real interest rates. With positive rates the infinite series representing the "discounted value of all future cash flows" converges to a single dollar value. With negative rates the series diverges: the "discounted value" of future cash flows is greater than their nominal value, simply because you're losing money with competing investments. The rational value of any investment that generates positive and predictable cash flows becomes infinite.

Right now the only thing holding a lid on equity valuations is the expectation that the Fed will eventually raise rates, and so cash flows from time periods > 2023 need to be discounted at positive rates. If that doesn't happen, or if they don't raise rates by more than the inflation rate at the time, things will go boom.

Two economists are sitting at a bar, one pulls out a checkbook and writes a check for $100,000,000 then hands it to the other economist. The second economist looks at the check, smiles, then hands it back.

The first economist calls the bartender over and orders a bottle of champagne. The bartender asks what the celebration is about, and the economist responds, "we just grew GDP by $200 million dollars."

This is not financial advise, but an investor myself, I'm on the other end of the spectrum. "Is it going to suddenly pop? Certainly! We just don't know when, how much and for how long. It could be june 2021, it could be 10 years after the Great Sino-Russian war of 2038".

The saying is that "As Long as the Music Is Playing, You've Got to Get Up and Dance." You can't -not- invest because it doesn't make sense and the valuations are insane because you could miss the dance or the encore.

That isn't sudden in the usual meaning. What is meant by the question "Are you going to suddenly die?"? If a safe falls on you death will be sudden but there isn't any reason to believe you will be around falling safes historically. You may have some hidden defect. Sure you will die eventually even if you were unaging, but what is usually meant is "Do you have any known fragility like say a weak heart, high risk of stroke, or a habit of using something volatile in dosage like speedballs or carfentanil? "

Not only this, but with the near zero interest rates and perceived impending hyperinflation, people are taking out massive margin loans to bet on assets. Archegos isn’t the only one, they just happened to get caught with a dumb position. When the interest rates kick up, we’ll likely see a dual effect here(stocks react, high rates mean it’s harder to service debt for speculators and actual companies) and a 2008-like scenario except our bad bet is on stocks instead of mortgages

We get articles on HN about once a week arguing that massive inflation is coming soon. I think all of these articles are misguided. With such low interest rates, the Fed can and will raise those rates to prevent inflation.

That interest rate rise will likely pop the bubble.

Unless you mean will it pop tomorrow, then yes that is unlikely. But the chances it pops “soon” seem quite likely. And it will be very ugly. I don’t know if we have ever seen a spring coiled this tight from money printing.

but what is a 'pop'? maybe ordinary swings in both directions due to various minor panics and manias and profit-takings that average out to a decade of nominal gains but depressed real returns?

'Pop' can also take the form of increasing inflation, making people take bigger risks for returns, leading to a bigger pop that is not coming soon. People saying this market can't sustain need to think about the inverse: what needs to happen for this market cycle to last 5-10+ years?

"The market can stay irrational longer than you can stay solvent."

2003 and 2009 style drawbacks but much worse. The SP500 has had 12 years of straight bull market, it's like an earthquake fault line that hasn't slipped in a long long time.

You don't have to choose one thing. A portfolio of two assets that are sufficiently uncorrelated can provide substantial returns over either one alone. They don't even have to be cointegrated. One of them could even have net negative returns, and it still works.

A split between equity and bonds still seems prudent, I think.

Exactly. Same with housing. They are not more valuable, the dollar is less valuable relative to them and likely will only get worse as equities and real estate are the good hedges against inflation, causing a positive feedback loop.

Higher interest rates would create an incentive for traditional savings, but would destroy companies (and gov) holding big debts.

I'm not sure where you are but housing over the last year is a real supply/demand market condition. They aren't arbitrarily being overbid 10%+ because the dollar is worth less suddenly.

Sure, but supply is limited in part because of the wealthy folks buying properties they will not use as a residence to hedge against inflation.

That real-estate is the least risky manner to protect wealth is a result of low interests rates and inflationary monetary policy. Printing as many dollars in the last year as there were in existence before, has perturbed a "normal" real-estate market. More dollars flying around means overbidding 10% is possible, especially since the additional interest is relatively negligible (wealthy folks will still take a loan in such conditions since rates are at rock-bottom).

I'll agree there is natural price pressure upward, but the recent acceleration is concerning, both in equities and real estate values.

Millennials were buying houses before all this too (I am and have) without this level of inflated prices (depending on where you are and how "free" the market is).

Well that's exactly it. In my area, inventory is scarce because of an influx of people who are used to paying an arm and a leg to live. In certain counties, prices are up 20-30% simply due to demand. Speaking with my own realtor, competition bidding is very common now. Rarely do you see a house go for asking or below asking.

Except measuring the value of money as something other than the ability to provide consumption (the ability to buy things you consume, rather than investments) doesn't make sense, regardless of how fashionable it is on this site to throw around the term "asset inflation".

What is your explanation for the explosion in asset prices over the last year, if not inflation? Do you think the assets have become fundamentally more valuable?

> What is your explanation for the explosion in asset prices over the last year, if not inflation?

Well, a few ideas immediately spring to mind:

a) Historically low interest rates are causing people to chase gains elsewhere. Again, people end up looking to the markets. This has been an ongoing trend exacerbated by...

b) For folks not on the margins, discretionary spending was severely curtailed last year. They had to do something with that extra cash. Many people, during a time of tumult, chose to save. This is only exacerbated a trend that started way back in 2008 due to similar post-disaster psychological scarring. Where did people put the money? Into the markets.

c) Wealth concentration means a huge amount of the cash floating around has landed in the coffers of the largest institutions and individuals. Those institutions aren't using that cash to buy chips at the 7/11. They're either i) saving it, which means putting it into the market, or ii) using it to buy up assets (e.g. acquisitions) which itself bids up prices.

In short: What's going on the market probably has absolutely nothing to do with what's going on on mainstreet.

Of course, that's been true for the last 10 years as folks on the fringes continued to predict hyperinflation post-2008. But, the great thing about disaster predictions is you can always just move the goalposts out...

1) Bonds and bank accounts are paying less than inflation, so to not lose money you need to invest in stock. That doesn't mean inflation is high rather bank accounts stink.

2) People figured out based on recent fed action that the U.S. has a policy of privatizing the gains and socializing the losses. Therefore stocks appear to not be risky, so people bought them up. The only reason you'd put money in a bank account rather than stock is stock can go down, but if you think the government will intervene to prevent stock going down, you might hold a greater amount of assets in stock, bidding up the price.

Tell-tales are all over the place. From explosion in asset prices world wide and cross-industry to micro-signals, such as goods coming in smaller packaging (for the same price) or slightly increasing grocery prices[0].

In my bubble, its mostly tinfoil-hat-wearing crypto-enthusiasts pointing at examples of how toiletpaper comes in smaller packages-for-the-same-price, so my view is skewed.

But its safe to consider all these as datapoints that indicate possible worldwide inflation is building up.

Slow inflation is the norm. Because if you have whole generations working and aren't experiencing growth things are deeply wrong. Not just "corporate lobbyists or those connected to officals have disproportionate influence" wrong but "masses of people working cannot improve their skills, processes, or products at all".

That is a very hard state to get even as a paranoid police state or literal aristocracy which views a minority of small farmer able to sustain their own plot as an existential threat. It is deeply unnatural in the "low probability" sense like your cat walking back and forth across a keyboard or swatting at it and writing passages of famous authors low.

One explanation is to look at the wood market. COVID restrictions have severely constrained supply and the wood suppliers are unable to keep up with demand.

Actually, measuring the value of money as something other than the measuring stick to compare capital assets doesn’t make sense, regardless of how fashionable it is to defend money printing by verysmart internet economists.

If your ability to consume food, water, shelter, and entertainment has not been impaired but you are complaining about "asset inflation" because you learned economics from message boards perhaps you are being haunted by nonexistent boogeymen and need to chill out?

There has been a big leap in technology over my lifetime. "Not impaired" isn't the target, if all the wealth gains weren't being directed to asset owners by asset price inflation then the people who were working to create them would be getting a bigger share.

I've done the obvious thing and bought assets, but it keeps getting harder and at some point maybe all the people who are working hard might notice that they are doing all the work and people with assets are getting all the benefits. The government should be more neutral on whether asset owners or workers get the benefits of work - the market is naturally slanted enough without it being further tipped towards asset owners.

You might be happy in stasis. But this is an age of wonders and the people who do the work to bring it about should be compensated roughly in line with their contribution. As would be happening if the government didn't keep leaning in with monetary policy to prop up asset prices relative to wages.

As a bonus, if the government did leave the market alone, people would probably work harder and there'd be more stuff to go around, even ignoring the fact that more of it would be distributed to the sort of people who work hard.

65.8 percent of americans own a home according to an internet search. (An asset). If you want to discuss wealth inequality, I don't think a term like "asset inflation" is necessarily the right way to go about it. Can't we just use terms like home affordability?

I just think reinventing the term inflation encourages sloppy fringe conspiracy thinking.

It's my understanding if the government didn't intervene in markets we'd get events like the great depression returning periodically, which probably are in nobody's interest.

We should really be discussing the right government policies or the wrong one, but I doubt the answer to the problems of our time is zero policy.

When you need to pony up an extra $100k for a down payment and your monthly payment goes up $300 for the next 30 years because real estate prices rise, is that not impairing your ability to consume other things?

It stinks that housing prices have gone up, but fortunately you can rent instead, which is accounted for in CPI measures of inflation.

I would think we could discuss the affordabity or unaffordability of homeownership without making up terms like "asset inflation" and falling into alternative fact rabbit holes about the collapse of U.S. currency.

Renting is not owning, and I question the utility of CPI’s method of measuring it that way.

My contention is increased real estate prices are affecting people’s lives in various ways, such as delaying families, not having families, moving people away from their networks, and at least allowing for a smaller portion of spending on other things in life due to a larger portion going into real estate.

Personally, I would label this asset inflation, but I don't know about the whole currency collapse thing.

I don't disagree with your main points but we have terms like Housing Affordability Index we can use to discuss this. We don't need to use imprecise terms like "asset inflation" which can mean different things to different people.

I wouldn't call some random person howling at the moon a fire alarm.

Never mind that online people have been predicting super inflation since at least 2009. I remember a Youtuber in 2009 that knew economics more than President Obama's advisors because Duck Tales did an episode on inflation.

But I guess by defining inflation as "stocks going up" the Duck Tales expert could have made it categorically impossible to be proven wrong since stocks tend to go up, further removing Duck Tales guy from the mainstream.

Consider that the Fed increases the money supply through debt. This means that for the money supply to increase, there needs to be an increasing amount of debt because eventually people pay back their debts and most of the money the Fed introduced into the economy disappears.

A Pandemic and multiple conflict zones were no more than a pot hole. The markets have pushed higher with no end in sight. The Fed and Treasury are making sure that if there is no one to buy stocks they will. There is no end to the support the Federal Reserve will shoulder for the markets.

With Governments around the world determined to never let the Economy fall or stay down even if it means directly sending money to the population and spending trillions at a moments notice to support Wall St there is no chance that over the long term the market will ever fall and stay down again.

Not even a WW or a natural disaster of the like we have never seen would keep the markets down. We would be naked, homeless and hungry and the market will continue to march higher. History is a perfect example of that.

i've been thinking the same thing for a couple years now. lots of people keep harping on doomsday scenarios, but it seems too many people have too much invested in the market for it to fail

I can never coalesce the whole pandemic and stock returns thing with the actual "fundamentals" of these companies. Yes - there was a pandemic, but the 5 largest companies in the index, Apple, Amazon, Microsoft, Facebook and Google, which make up nearly 20% of the index all had insane revenue growth. Amazon nearly doubled it's profits, Google growing as much as 30%.

When every other investment vehicle, except maybe housing is cratering you have a one-two where stocks looks great to invest in, and are much better than everything else. If it were to ever pop it would be because other investment products started to get much healthier - which to me isn't a bad thing.

The stock market is about future expectations. As soon as you know that, the last year makes perfect sense. Oh no, a plague = crash. Oh wait, it will be shitty for 6 to 24 months but actually not that bad and people are still buying stuff just as much as before = Boom.

Stock market returns make sense only when you realize the currency is actually just losing value. All currency is being devalued so you don't see it in currency pairs but scarce assets go up quickly.

I think that given how vast is USD influence, currencies all over the world will lose their value with dollar. But not every currency, economies that rely on mining natural resources more should have their currencies better against USD.

Why would mining help? Resource extraction is the low end of earning potential. You mostly need the terrain and a willingness to pollute to break into it. It isn't that scarce. Industry makes much more than resource extraction and advanced services make more than industry.

When S&P plunges more than 10%, buybuybuy. 30%? Shit go full margin and back up the truck. I’m sitting on 2x since Dec.

Protips. Saas is the thesis. Long term solar is a 100x-1000x easy-ish bet. Capture is “good enough”, we are going to solve storage. Transmission will significantly collapse into storage. Game will change. The entire energy game.

Reminiscent of the dot com boom. People said "this internet thing really looks like it's on the up and up" and they were right. What they didn't understand is that investing in 'pets.com' didn't mean they were investing in the internet.

Yes the solar industry could probably go up 100x. No, the companies we're investing in today won't track that.

It's been a long, long run. If you ignore the drop from last March that was recouped within months, it's been a strong ramp ever since the second half of the Obama presidency. Vanguard tells me I've done better than 16% over that period, just invested in the boring VTSAX index fund.

I might agree that general stock market prices are quite high, but arguing that "they went up 15% in 6 months" doesn't seem particularly strong. That has occurred historically, and doesn't automatically mean it's overpriced.

Stocks market returns only represent the return of the companies that are listed on stock exchange. If the economy stagnates overall but the small (unlisted) companies suffer while the big (listed) ones boom, then the stock market returns increase in a stagnating economy but it makes sense.

The problem here would be the belief that stock market is a mirror of the main economy. Personally, I believe the stock market represents very well the interest of the richest capitalists.

Against a basket of currencies, the US dollar index is approximately 10% lower than it was from the start of the pandemic. Pointing to the fed money supply chart as evidence is woefully misleading.

Counterpoint would be that against "a basket of assets" it is decreasing in value rapidly.

The EUR is probably tanking just as fast. What you are doing is like saying "shipping prices for steel have not increased, because the price to get a kilogram of steel across the ocean is hardly more than the price to get a kilogram of coal across the ocean".

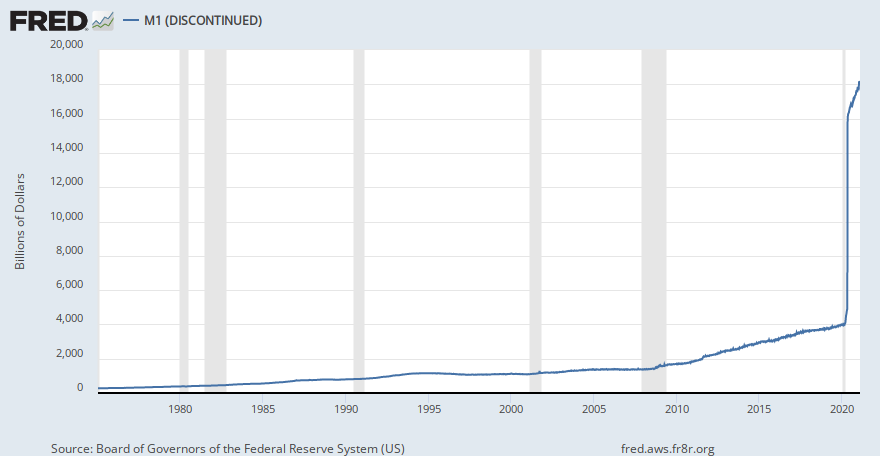

Much of the increase was just banks relabeling their M2 money as M1. This happened when banks stopped penalizing people from withdrawing from their savings account more 6 times a month.

{kind=link}