Most people are unaware of the true mechanism of money creation, therefore don't understand how the current mechanism and its (lack of) constraints affect society, therefore don't see the potential for societal improvement through systemic change around money creation and allocation.

Prof Richard Werner is worth listening to on this topic. [1]

I'd also recommend Steve Baker's heroic speech in UK parliament. [2]

It seems like leverage has shifted from the central banks to commercial banks over recent decades, and indeed there has been massive consolidation of power in the commercial sector. The central bank seems more like an insurance proxy for the tax payer to the commercial bank, as evidenced by the 2008 rescue packages.

An aspect of this I wonder about is that many years ago a bank account is what you opened when you explicitly wanted to lend money to the bank to earn interest. But these days a bank account is pretty much mandatory for any sort of normal existence.

One thing that is astonishingly glossed over again and again is energy. There is no activity, no economy of any sort without energy. Energy availability therefore is absolutely central to any economic activity. Energy availability is not infinite, or infinitely elastic to demand. You cannot either infinitely yield more output from a given amount of energy. In last resort, we could say that all money is an energy debt (every dollar amounts to some energy quantity that varies). Making untenable promises by printing large amounts of money doesn't change this (promising that in 20 years, we'll have x% more energy than today doesn't help making this actually happen).

In a finite world, you can't grow economy infinitely, period. Frigging laws of physics.

Steve Keen is doing some interesting stuff incorporating energy into economics - here's some of his older stuff - http://www.debtdeflation.com/blogs/2016/08/19/incorporating-... - if you google a bit I think he's developed that further (probably some of his lectures which are available on YouTube are where the newer stuff would be - I'm not sure if he's published much of it yet)

Apparently you didn't make the effort to read the article I linked to. You're talking the usual, wishful-thinking nonsense that'll bring us into the entropy wall full speed, real soon now.

Yep, this is exactly the point economist Julian Simon made in his essay, "Can the Supply of Natural Resources - Especially Energy - Really Be Infinite? Yes!" [1]

This exert from the conclusion sums up his argument well:

> Incredible as it may seem at first, the term "finite" is not only inappropriate but is downright misleading when applied to natural resources, from both the practical and

philosophical points of view. As with many important arguments, the finiteness issue is "just semantic." Yet the semantics of resource scarcity muddle public discussion and bring about wrongheaded policy decisions.

This is utter BS. It relies on bad analogies and not physical reality. The example given (copper) is absurd; recycling implies using energy (and disposal of waste heat), therefore you substitute a resource (copper ore) for another (used copper and energy). The analysis supposes that every resource is substitutable (they aren't), and that energy is infinite (it isn't).

We don't know for sure that the universe isn't infinite, but we do know that it is at least tens of billions of light years across. We aren't going to run into actual laws of physics making growth impossible for a long fucking time.

Only provided we leave earth and we harvest energy in a more efficient way. One of the reasons I'm supportive of renewable energy is not for environmental reasons; rather, that it's energy that would otherwise have been lost. Extracting hydrocarbons removes the total amount left, but extracting energy from sunlight doesn't lower the amount of sunlight that'll be emitted. Renewables are a responsible long-term energy play, and not just for the planet's health.

Yeah sure, if we suppose that we have nearly infinite resources (energy and material and science to propel billions of humans off the Earth and across the galaxy), we have no short-term resource problem. However we're already constrained (average OECD countries energy availability has been falling since 2006), so you can't exactly hand-wave the problem away.

You’re right, but the transformation is subject to the 2nd law of thermodynamics. The useful work you can do is diminished, and you’re left with entropy. Energy is neither created nor destroyed, but we don’t care about how much waste heat we have available, because nothing can be done with it.

This should not come at a surprise as money really is debt.

Say you get a loan of 100$: now you have 100$ more to spend...but your creditor can still factor his/her credit (sell it at a discount) and spend that sum.

That initial 100$ can be spent twice (minus discounting factor).

Of course that loan needs to be repaid at one point.

But what if you keep on making new debt to repay the previous debt?

And what if the credits you generate have a particular utility for your creditors (eg. government-bonds for banks) so that you get 0 or even negative interest rate?

You got really close to creating money. The difference between different types of debts and money is rather quantitative (interest rate) than qualitative: https://en.wikipedia.org/wiki/Near_money.

Yes, learning how banks create money for me was a huge turning point in realising most of what people think they know (and what I thought) about money, debt and economics is actually wrong. That the money supply grows when banks lend and contracts when people pay the debt down is a big point to get your head around.

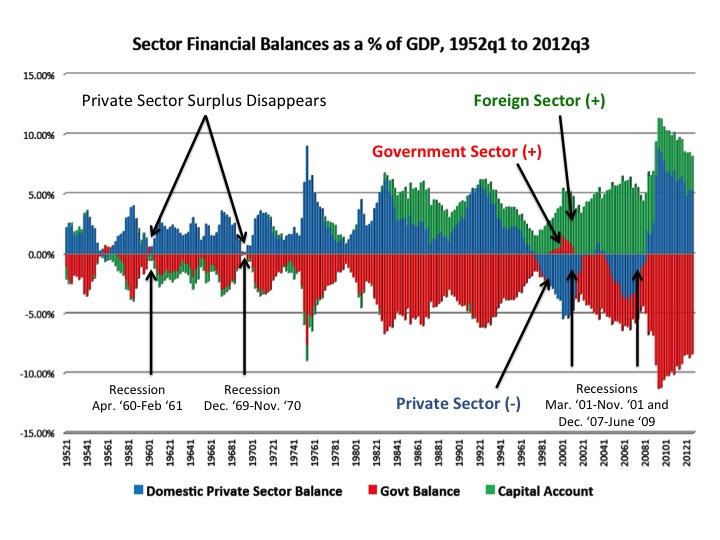

The other big one is the national accounts and sectoral balances - see [1] for a much more detailed run-down.

To summarise, take the definition of GDP:

(1) GDP ≡ C + I + G + (X – M)

where C is household final consumption, I is private investment including inventory, G is Government spending, and (X-M) are net exports.

Add net external income flows (FNI) to (1) and you get GNP:

(2) GNP = C + I + G + (X – M) + FNI

Subtract total transfers and taxes from each side:

(3) GNP – T = C + I + G + (X – M) + FNI – T

Collect terms by sector (private, Government and External)

(4) (GNP – C – T) – I = (G – T) + (X – M + FNI)

Then we can simplify - (GNP - consumption - taxes) is equilivalent to private saving (we’ll call that S), and (X - M - FNI) is called the Current Account Balance (CAD):

(5) (S – I) – (G – T) – CAD = 0

or (6) (S – I) = (G – T) + CAD

What this means is that by definition, if your external sector is balanced, a Government budget surplus must reduce the net assets of the private sector by exactly the same amount as it is in surplus. With a trade deficit and a Government surplus, the private sector’s net assets are reduced by the sum of those.

This is quite clear graphically too [2].

So the end result is that you can only have economic growth when the Government is running a surplus and the private sector is in balance or deficit through money creation from banks. Is relies on people borrowing more and more money - but because equal amounts of debt are also created (no higher net wealth), eventually the sector in aggregate can’t borrow any more, and the system falls apart (the second derivative of credit growth dropped a little while before the GFC, which is how some non-mainstream economists predicted that it was coming).

But at the end of the day, this means a balanced or surplus Government budget is actually bad for the economy by definition unless you have a big trade surplus (like Germany for instance), because it’s sapping the private sector of wealth.

Do you have to start taking a more nuanced view of Government debt, when Government debt actually represents the net actual savings of the private sector!

> But at the end of the day, this means a balanced or surplus Government budget is actually bad for the economy by definition

Not necessarily. You're thinking in nominal terms. There could be the same money supply but nothings prevents producing more and consuming more. Also beware the trap of equating fiat money with wealth: Zimbabwe government's deficits are also private assets...

There needs to be enough money to purchase the goods and services produced. Yes, there is some multiplier from monetary velocity (one persons expenditure is another’s income, so the same money can be spent multiple times), but the supply still needs to grow to not experience deflation, and that can only come from a trade surplus, bank created money (private debt) or Government deficit spending, by the definitions above. And since lending in the private sector must create debt too, the private sector cannot increase its own net financial assets.

Zimbabwe is well understood by modern monetary theory. If you look at what actually happened, it’s not an argument against the mathematical fact that a Government must spend somewhat more than it taxes to have a stable economy in the presence of a trade deficit (don’t make the mistake that many do when confronted with the fact that a currency issuing Governmment is not fiscally limited - of course that doesn’t mean that the Government should spend unlimited money. Of course if its spending pushes aggregate demand enough above the supply of goods and services produced in the economy you’ll have inflation, and even hyperinflation if you push enough - but on the other side, some of the most successful Government surpluses (apparently ‘responsible’ Government budgeting) without trade surpluses have preceded many financial crises).

Zimbawbe’s economic woes started when farms were confiscated, leading to huge unemployment (80%!) and a huge supply shock with food production reduced by a massive 35%. The Government then depleted foreign reserves by using it to import food. In response, the Government overspent domestically, partially in an attempt to buy political favours - and not investing in productive capacity. Of course hyperinflation happened!

Venezuela has similar issues (big supply shock due to Government policy), as well as the added problem of attempting to keep up a fixed exchange rate to the US dollar (fixed exchange rates always fail eventually).

> And since lending in the private sector must create debt too, the private sector cannot increase its own net financial assets.

In this respect it is identical to the logic of real world deficit spending in the developed world, where (ceteris paribus) each and every dollar spent is matched by the issue of government debt (with the "net financial asset" monetary base being adjusted independently of current period G by a separate institution in order to hit a target interest rate).

But the wealth of a nation is not a growth in what MMT calls "net financial assets" (i.e. currency with no debt obligation attached), the wealth of a nation is a growth in goods and services sold. The fact I have to repay a loan with interest in ten years time does not mean that I am less likely to generate goods and services with it this year (if anything, it encourages me to do so, because I need to generate a profit to repay the loan). Provided lending continues to grow, the amount of currency available to purchase the goods can continue to grow even in trade deficit and budget surplus (which might in some circumstances represent a useful counterbalance to excess lending growth) whilst holding monetary velocity constant.

What actually matters is not whether the money pumped into the economy has debt attached, but whether it's spent creating new assets/services which the public wishes to purchase or spent bidding up the price of existing assets or production processes. In theory (but not always in practice) money which is in aggregate lent into the economy is more likely to be invested in production to meet repayments than money spent into the economy.

> So the end result is that you can only have economic growth when the Government is running a surplus and the private sector is in balance or deficit through money creation from banks.

Not that fast. The catch is that all those equations are nominal, and they have an incredibly complex interaction with the real economy.

>Government debt actually represents the net actual savings of the private sector!

Excuse me, but when Federal Reserve conducts QE and buys 1 trillion of freshly issued government debt, what does it have in common with actual savings of the private sector? Who saved that paltry trillion? :)

Yes, QE is interesting. Definitey goes against the “Government must tax before it can spend” idea. Remember the Fed is part of the US Government sector, so spending as a result of QE should go into the private sector, minus what is taxed back later.

Government securities generally represent savings because the Governments are generally legally required to match deficit spending with bonds, etc. QE was a bit of a departure from the norm (perhaps only temporarily though) and shows what modern monetary theory says - that it isn’t really necessary, not is it necessarily inflationary (this is because all spending carries inflationary risk, and inflation has to do more with aggregate demand than money supply etc. - and the most generally anti-inflationary force is actually taxation)

I have a different view. Unfortunately it's not possible to make a real scientific experiment to validate your or my assumption.

My thinking is that QE is quite inflationary.I think that after 2008 crisis we were expected to have a long period of strong deflation (let's say, with prices falling 4% each year, for 8 years straight), but QE reverted that and we had 1% of inflation or something like that instead. So, formally we are in "mild inflation" ground, but in fact the QE effect was quite dramatic. We just can't observe it because we don't have a "control group economy".

Well, all spending carries inflation risk - what really matters is what aggregate demand is like and how much spending and taxing alters that. Certainly QE could be inflationary, but as it was it was mostly just buying back securities it was mostly asset neutral so shouldn’t have done much (just like issuing Government securities to match deficit spending (just in reverse) - it doesn’t actually alter whether deficit spending is inflationary or not since there is a quite liquid market for those assets so they’re very similar to cash).

It is considered to have inflated prices of certain financial assets though (shares etc.)

stephen_g, if you are interested, then I wrote a very simple scenario of how QE could (and IMHO did) spill over into "real economy" here -- https://news.ycombinator.com/item?id=16606140

You do know the Federal Reserve is not actually federal and is owned by private banks right? Perhaps there is some definition of US government sector I'm not aware of.

That's a common misconception. It's technically a soft of public-private hybrid, but the "ownership" by private banks is purely symbolic. The system is considered "independent within the Government", not independent of the Government.

The Federal Reserve's governors are appointed by the President and confirmed by the US Senate, and it derives all its authority only from the Federal Reserve Act. The organisation is accountable to the Government Accountability Office as well.

Most central banks though are just directly owned by the Government of the country, even if they are meant to operate independently.

The "independence" of central banks is generally a bad thing though - the point is supposedly to "depoliticise" them but really it's just an attempt to remove any democratic control of them.

Your first paragraph is just flat wrong. I know quite a bit about the Fed, and I'd like you to cite your source on both the "public-private hybrid" part and the "purely symbolic" part. Neither are true, unless you consider 6% of trillions and trillions (after expenses) "purely symbolic". I have no idea where you get the hybrid part. No government owns shares of the fed.

Also, for your information, the GAO audits are anything but accountability. After finally getting the GAO audit part passed in 78 there were so many limitations on thier audits as to make them so piecemeal they are more of a rubber stamp than anything. (Not to mention a few times when it got out the Fed destroyed source documents)

Don't call something a common misconception when you don't have a more solid understanding of the subject please. The common misconception is that they are federal, not the other way around.

QE is just repricing risk. It doesn't really have any real economic impact. But when you're in a severe depression people will try anything.

BTW it's not true at all that economic growth requires a surplus. In fact often the case is the opposite. I strongly recommend people who want to understand this read up on Modern Monetary Theory. Once you understand how this stuff really works (yes Banks create money they are not dumb intermediaries sand fractional reserve banking is a myth) it will help a lot to understand much of what is not reported on the news.

>QE is just repricing risk. It doesn't really have any real economic impact.

That's where things get interesting.

Let's imagine, for a simplicity sake, that there are 3 types of assets -- government debt, apple stocks and tesla debt.

If I'm sitting on my 1 trillion of government debt and I want actually switch to apple stocks (or maybe just get dollars and eat pizza and drink margaritas), I need to sell it to someone who will put his trillion into government debt. So, for me to "untie" my 1 trillion in government bonds and free it for consumption, someone has to "tie" his trillion dollars into it.

Now, fed enters the market and buys that 1 trillion from me as a part of QE. It does not need to sell his apple stocks or delay consumption and save that 1 trillion.

I now have dollars in my account, and can use it to buy, say, trillion of tesla debt, because I love Elon Musk.

Musk, in turn, can look at the market and observe that it has a huge appetite for tesla debt, and it was not the case one year ago. So maybe it make sense to issue one trillion dollars worth of bonds and build Gigafactory-2 and another car factory, and he does exactly that.

Are we still sure that when Gigafactory-2 is being erected and people are hired for a second car factory, "QE have no real economic impact"? It's not obvious to me.

The only thing that changed here is you swapped one type of money-like asset for another. Previously you owned bonds and now you have cash. Anything you could do before you can still do. (You can pay for stuff like factories with bonds.) I don't see why you think you're suddenly richer. QE has no impact on your wealth because you're just swapping similar assets. Now you can argue that it does send a message to the animal spirits leading to your risk preferences to change (seeing the Fed act so boldly makes you more likely to invest) which leads to a rising stock market and eventually a general "wealth effect" ... But this is kinda voodoo magic and no longer a quantitative analysis even if it's real.

(BTW in reality the market for government debt is very liquid. What you're really describing hate it's liquidation risk. It becomes an issue for more think traded instruments but not for bonds.)

Well, yes. Since Fed is not making pizzas and margaritas, it can only swap one asset for another, it can't mix you a decent margarita.

And if Fed will go out and just buy the whole outstanding float of GOOG, AAPL, TSLA, FB and NFLX with freshly minted money, it would be, bingo, "swap of one asset for another".

Don't you think that asset swap like that will somehow affect the general economy?

EDIT: damn, let's go _really_ extreme. Fed can basically swap all the government debt with dollars. All the 21 trillion of it, in a single asset swap. Click-click and boom, USA is debt free, no more interest payments, hooray. Dont you think such swap will have some real-life repercussions? If it will, how it's different from QE?

> Are we still sure that when Gigafactory-2 is being erected and people are hired for a second car factory, "QE have no real economic impact"?

I'm pretty sure it does have an economic impact on growth. The argument according to which it wouldn't make sense when you're at or near potential GDP, but when you fall enough below that - as in a big recession - increasing the money supply definitely has an impact. Then, it can be argued if the impact is good or bad in the long term - eg: will people create useful Gigafactories, or will they build unsustainable McMansions? But the impact is there.

While informative I think that this article is somewhat misleading as it omits any discussion that the reserves described are, in fact, fractional reserves.

It seems quiet ironic that Bitcoin/Cryptocoin advocates claim the minting and production using algorithms like Satoshi's BTC will be better than fiat when it just creates a new oligarchy... easier to co-opt due to the consolidation of control within the cryptocoin ecosystems.

Banks and the finance sector took note of BTC prior to 2014, and with the way BTC is produced anyone with enough capital entering into BTC - especially during the first few years would be in a position to take vast amounts of BTC at low cost and simply wait and attempt to convince other people to exchange their wealth for BTC which due to how the supply begins to be cut off, serves to enrich the minority of oligarchial squatter-speculators.

Bitcoin is often misunderstood as "deflationary" yet checking the math under the hood and we see that's a half truth. The supply inflates every 10 minutes, and for the first few years Bitcoin was hyperinflationary, granting a small group of users the majority of the supply.

Satoshi Nakamoto

Thu Jan 8 14:27:40 EST 2009

I made the proof-of-work difficulty ridiculously easy to

start with, so for a little while in the beginning a

typical PC will be able to generate coins in just a few

hours. It'll get a lot harder when competition makes the

automatic adjustment drive up the difficulty.

first 4 years: 10,500,000 coins

next 4 years: 5,250,000 coins

next 4 years: 2,625,000 coins

next 4 years: 1,312,500 coins

____________________________________________________

____________________________________________________

One important point: if we actually include all 7 billion

people on the earth, most of whom have zero BTC or

Ethereum, the Gini coefficient is essentially 0.99+. And

if we just include all balances, we include many dust

balances which would again put the Gini coefficient at

0.99+. Thus, we need some kind of threshold here. The

imperfect threshold we picked was the Gini coefficient

among accounts with ≥185 BTC per address, and ≥2477 ETH

per address. So this is the distribution of ownership

among the Bitcoin and Ethereum rich with $500k as of July

2017.

In what kind of situation would a thresholded metric like

this be interesting? Perhaps in a scenario similar to the

ongoing IRS Coinbase issue, where the IRS is seeking

information on all holders with balances >$20,000.

Conceptualized in terms of an attack, a high Gini

coefficient would mean that a government would only need

to round up a few large holders in order to acquire a

large percentage of outstanding cryptocurrency — and with

it the ability to tank the price.

With that said, two points. First, while one would not

want a Gini coefficient of exactly 1.0 for BTC or ETH (as

then only one person would have all of the digital

currency, and no one would have an incentive to help boost

the network), in practice it appears that a very high

level of wealth centralization is still compatible with

the operation of a decentralized protocol. Second, as we

show below, we think the Nakamoto coefficient is a better

metric than the Gini coefficient for measuring holder

concentration in particular as it obviates the issue of

arbitrarily choosing a threshold.

...However, the maximum Gini coefficient has one obvious

issue: while a high value tracks with our intuitive notion

of a “more centralized” system, the fact that each Gini

coefficient is restricted to a 0–1 scale means that it

does not directly measure the number of individuals or

entities required to compromise a system.

Specifically, for a given blockchain suppose you have a

subsystem of exchanges with 1000 actors with a Gini

coefficient of 0.8, and another subsystem of 10 miners

with a Gini coefficient of 0.7. It may turn out that

compromising only 3 miners rather than 57 exchanges may be

sufficient to compromise this system, which would mean the

maximum Gini coefficient would have pointed to exchanges

rather than miners as the decentralization bottleneck.

Conversely, if one considers “number of distinct countries

with substantial mining capacity” an essential subsystem,

then the minimum Nakamoto coefficient for Bitcoin would

again be 1, as the compromise of China (in the sense of a

Chinese government crackdown on mining) would result in

>51% of mining being compromised.

Anyone can mine. Anyone can earn bitcoin. Early adopters have been rewarded, sure, but the distribution of bitcoin has been steadily increasing. The vast majority of the world is able to exchange their local currency for bitcoin should they decide to take that risk.

How exactly do you propose a decentralized currency controlled by no one bootstrap itself?

The reasonable choice would be to mine a fixed amount of coins per year over ~100+ years not have a perimid scheme designed to artificially reward early adopters, and simulate a pyramid scheme.

And that's sidestepping the issue with ~1/5 of all possible coins already being lost.

It's likely that there won't ever be a single cryptocurrency that solves all the messy and complex problems of our global financial systems. Bitcoin is certainly far from delivering on that promise at the moment. It has however delivered a significant improvement in providing a trustless, secure, fault tolerant and immutable environment in which to implement a clean slate in monetary policy. Ethereum evolved this from a ledger of transactions to a ledger of computational states, and off to the races we've gone in using these as inspirations toward improving the broken qualities of our modern financial services industry. Factom offered a different take on inflation and deflation, dozens more tinker and toil to get it right. Transparency has improved, regulations have begun to take shape, and its just the first inning.

That presumes there's a pressing reason to pay thousands of dollars for a bitcoin. Which seems absurd to me. If it ceased to exist, my life wouldn't be affected in the least.

The person I was replying to claimed $1000 was an absurd amount for a bitcoin. I was merely pointing that 1 btc is an arbitrary amount of satoshis.

Anyways, my point stands: how do you expect a grassroots currency to bootstrap itself? Of course the first miners had it easy, no one took the currency seriously back then.

Regardless of the numbers, the other posters on this subthread are making an important point: too much wealth concentration deters new adopters.

Think of it in terms of the Ultimatum Game [1]: when faced with a new system of wealth distribution, potential new participants not currently within the system have two choices. They can choose to trade something they possess that would be of value to the existing participants (labor, wampum, or $USD, for example) for the new currency. Or they can say "Fuck you, I'm not playing in your sandbox."

The challenge for Bitcoin is that only ~0.3% of the population is involved in it, but the amount of money you have to spend to get a tiny fraction of the wealth that early adopters got just for showing up early is ridiculous. Under those conditions, the incentives for the remaining 99.7% is to say "Fuck you, I'll stick with my dollars". Or, alternatively, to create new currencies with their own pyramid schemes in the hopes of replicating Bitcoin's success.

Too little reward for early adopters and the new currency never gets adoption. Too much, and its adoption stalls out before it reaches a critical mass of the population. Ramp up the inflation rate later, and you can get continued growth after adoption, but at the expense of overall trust in the currency. It seems like you need a steady stream of broken promises, buried history, and disaffected outsiders to both gain adoption of a new currency and continue its growth.

(Interestingly, fiat has the same problem now: a significant number of people believe their chance of amassing significant wealth is near-zero within the current system, which is one of the major factors driving adoption of Bitcoin. They're effectively saying "Fuck you, I'm not playing in your sandbox" to the financial system of the developed world. But the other posters in this thread are pointing out that this problem is not unique to fiat, and that Bitcoin itself has this problem too, as does every other attempt to coordinate a new store of value.)

Database tokens acquired though a software game of number guessing (Satoshi's PoW algorithm), rewarding less and less as the number grows larger would be more akin to fools gold.

Here is a simple way to demonstrate the point of the article. If I deposit $100 in a bank, the bank can lend out around $90 to someone else (fractional reserve banking). That person now deposits the money at another bank, and the "money supply" is $190 instead of $100.

On the other hand when a central bank "prints money", they use it to buy assets with an equivalent value, so there is no net transfer of wealth done by the central bank. That assumes they don't affect asset prices, which not a great assumption.

The way central banks affect the money supply is through interest rates to change the supply and demand of private loans that banks make, which indirectly affects the money supply.

> If I deposit $100 in a bank, the bank can lend out around $90 to someone else (fractional reserve banking)

This is the textbook explanation which the article strongly rejects. In practice the bank will lend out as much as possible - it is not effectively constrained by reserve requirements since it can and will simply borrow the difference. What constrains it is market forces (the demand for loans, and their profitability), and financial regulations, and finally the interest rates set by the central bank.

If a retail bank believes it can turn a profit by lending money borrowed from the central bank, in compliance with the law, it will do so until it exhausts the opportunity. Consumer deposits are irrelevant.

Exactly. There is no reserve limit: any pretense of that was washed away once sweep accounts became standard.

Banks lend as much as they possibly can, and then a bit more, and then expect the taxpayers to pick up the pieces when it all falls apart.

The irony is that there need not be a reserve ratio: if we just adopted duration-matched banking, where a bank had to demonstrate it had ownership of a given dollar it was lending for the duration it loaned that dollar (e.g. via a CD) it would be fine.

This is the fundamental problem with banking, and I don't understand why no one talks about it. Banks are lying about having money they don't have (i.e. they are promising the same dollar to more than one person at the same time). If we forced them to just stop lying it would all work out, and there wouldn't be any need for a reserve ratio.

As others have said, that is a textbook model of banks that describes how banks haven’t worked for at least a century (if ever?). That’s called the ‘money multiplier’ model, and it’s a myth. Even ‘fractional banking’ isn’t really a valid explanation. How banks work is called ‘endogenous money’, but one economist is trying to change that to the more friendly and self explanatory “bank-originated money and debt.”

The most amazing thing about how banks actually work (see the article) is that they don’t need any deposits to lend. Thus, how much a bank can lend is utterly independent of the amount of deposits they have. (Of course, deposits are useful for liquidity for interbank transfers, but the bank can just borrow reserves from other banks or the CB if it needs). But lending creates deposits with an equal amount of debt.

The other thing to remember is that deposits are a liability to the bank. A bank couldn’t lend out deposits because it wouldn’t balance out in double entry bookkeeping - even if it created the debt as an asset, it needs to create the matching deposit, so now you have two liabilities (deposit lent from, deposit for the person lent to) and one asset (the debt), which doesn’t sum to zero. Whereas creating the asset (mortgage / debt) and a matching liability (deposit) does.

Apparently my answer is worse than the guy who thinks "The fed is literally giving asset holders free money" and the guy who makes a pitch for Bitcoin. Whatever. Utilize your downvote cartel however you see fit I guess.

Regardless of whether the loans are linked to individual deposits or borrowed from other banks, I was just trying to communicate how commercial banks could increase the money supply without input from the central bank. Nowhere did I claim the reserve requirement and monetary base were the limiting factor of the money supply (in fact the last sentence says supply of loans is influenced by interest rates). This is just what figure 1 depicts in the paper. The direct quote from the conclusion of the paper is "Most of the money in circulation is created, not by the printing presses of the Bank of England, but by the commercial banks themselves."

Furthermore I claimed that central banks affect the money supply via rates, which is supported via the conclusion as well: "The Bank of England is nevertheless still able to influence the amount of money in the economy. It does so in normal times by setting monetary policy — through the interest rate that it pays on reserves held by commercial banks with the Bank of England. "

“QE involves a shift in the focus of monetary policy to the quantity of money: the central bank purchases a quantity of assets, financed by the creation of broad money and a corresponding increase in the amount of central bank reserves. The sellers of the assets will be left holding the newly created deposits in place of government bonds. They will be likely to be holding more money than they would like, relative to other assets that they wish to hold. They will therefore want to rebalance their portfolios, for example by using the new deposits to buy higher-yielding assets such as bonds and shares issued by companies — leading to the ‘hot potato’ effect discussed earlier. This will raise the value of those assets and lower the cost to companies of raising funds in these markets.”

The fed is literally giving asset holders free money at the expense of people trying to save in traditional ways (savings accounts). They buys whichever bonds they decide which then enables the holders of those bonds to collect free money. All the new money slowly works it’s way into the rest of the economy, inflating away the value of our savings.

Crap like this is precisely why bitcoin will succeed. Eventually people will realize what the Central Banks are doing and will decide they’ve had enough.

It's not "free money". Investors get the money by selling assets. But it might be at a better price than they could have gotten elsewhere.

One lesson is not to use a savings account as the only place to keep your money. Anyone who has looked at interest rates in the last few decades already knows this.

Another lesson is that it would be a lot more fair if the Fed had a way to boost the economy that involved giving money to normal people. This gets talked about as "helicopter drops" but never happens. (It probably requires an act of Congress.)

It is free money. If you bought a bond for 30 years today, and the fed came along and said they’d give you what you paid for the bond plus 20 years of interest payments, how is that anything other than free money?!

Without conflating savings with investment, how would you propose an individual save money?

> It is free money. If you bought a bond for 30 years today, and the fed came along and said they’d give you what you paid for the bond plus 20 years of interest payments, how is that anything other than free money?!

If you had to put it away and couldn't use it for 30 years, it's not really free, is it? It cost you 30 years of not being able to use it. Plus you're taking inflation risk, default risk, depending on the bond you might also be taking liquidity risk, etc. You're talking out of your ass dude.

Ummmmm, you’ve got it around the wrong way friend. The central banks are buying the bonds. You had already taken on the risk of buying the bond. The fed then came and said, “I’d like to buy your bond and give you 20 years of interest payments on top of your principal.”

If you have a 30 year bond and hold it for 10 years then you get 10 years worth of interest payments. When the fed (or anyone else) comes, they buy it at the market price of a 20 year bond (30 year bond after 10 years is a 20 year bond). You don't get any interest payment on top of that. It's still not free money, you took the risk of holding a 30 year bond for 10 years. And it's not "on top of the principal". They don't give you the principal for your 20 year bond, they give you the market price. Which fluctuates, and hence you're taking a risk and being rewarded for it.

Suppose there is a new issue zero-coupon 10 year bond with par value of $1000. The price for that bond is roughly $750 which gives me a 6%/yr return at maturity.

I buy it, and the fed comes around 1 month later and decides they want to do QE. They decide the 10 year yield is what they want to target so they go on the market and start buying bonds. The price goes from $750 to $900 in a short time.

I can now take my bond I purchased for $750 and sell it for $900 if I desired — this is the same as returning my principal plus a few years of interest payments after having held the bond for just a few months.

What? I said the initial price of the bond was roughly 750$ which represented a 6% yield.

900 comes from QE. If the fed wants a 10 year interest rate of 1%, they would buy bonds on the market until the price rose from 750$ to 900$. And that is exactly what they did with QE 1-3.

No wonder they got away with it... no one here even understands how QE worked.

If you buy a 10 year bond for $750 and wait for 1 month, now you have a 9year,11months bond, which will have a price slightly below $750, and that's what the fed will give you for it. YOU made up that they will pay $900, but they won't.

But.... you're the one who's complaining that you missed out of assets booming due to QE. So surely if anyone doesn't have a clue it's you, right? I did quite well over the past decade.

By your definition, any price rise in any asset is free money for whoever holds the asset. That's... kind of true, in a way, I suppose, but not a very useful way to look at it.

What you seem to be either missing or sweeping under the rug is that the holder has to sell the bond in order to get the money. Your description is therefore rather odd for the reality of the situation. It looks like you wanted to find the most outrage-inducing description that had some faint correspondence to the situation.

> The fed is literally giving asset holders free money at the expense of people trying to save in traditional ways (savings accounts).

If you believe this, isn't the rational thing to use your dollars to buy assets?

I think you're betraying a deep mis-understading of how money works. QE has been raging for 10 years, but inflation is incredibly low (2.5% US, 1.5% EU). In other words, even though you claim that the FED "gives asset holders free money", when you hold cash you're not really losing purchasing power. How do you square the two things?

Very simple. For everything that could be produced in China or, say, Vietnam, you have, essentially, a deflationary backstop. No matter how many mp3 players you want to buy, chinese will deliver without rising prices, since they have a capacity and happy to utilize it.

For stuff like real estate, or stocks... bloomerg reported yesterday that "FANG Rally Is Outpacing the Heyday of the Tech Frenzy" [0]. Stock market was and still is a good place to be for last 9 years, and while economic recovery was slowest since Great Depression [1], stock market roared for some reason. Hmmmmm..

It's not that simple. The word "assets" is the wrong word (and I know, you didn't pick it). What actually happened was that there were two kinds of assets, safe and... not so safe. And when the bottom fell out on housing, people got out of the stock market too. Where did the money go? Some evaporated, as people found out that their assets weren't worth as much as they thought they were. A bunch of the rest went into bonds, especially US Treasuries, which were regarded as the safest asset out there.

The Fed responded by buying a bunch of treasuries (QE). That drove the price up. If you happened to hold treasuries when the Fed did this, you made money. On the other hand, everyone else on the planet was also buying treasuries, so the price was going up anyway - the Fed just made it go up more.

So some people sold, because the price was high. Some did it to cash in the price rise. Others did it because, going forward, the rate of return was dismal for the next X years. Those who sold had to put their money somewhere. Where would they put it. Not in treasuries - that was what they were selling. So they were getting out of treasuries, and had money to buy other things. That's what the Fed intended.

But it's not just QE. It has always been a good strategy to hold bonds when interest rates fall, because the price of the bond moves in the opposite direction of interest rates, and the longer the bond duration, the further the price moves.

Why did the Fed do this? A few paragraphs ago, I said that some money just evaporated. Well, "some" here means four trillion dollars. So the Fed used QE to create four trillion dollars and pump it back into the economy, which kept the whole thing from seizing up in a real Great Depression. Whether people holding treasuries at the time made a bit more money than they would have is beside the point.

So freejulian is wrong in what he's implying, that there was some conspiracy of evil bankers to transfer money to the rich. But he's right that, when this came down, holding bonds was the right move. (But by the time QE started, the big gains had already happened.)

> If you believe this, isn't the rational thing to use your dollars to buy assets?

If you have leftover capital after consumption, then yes.

>I think you're betraying a deep mis-understading of how money works. QE has been raging for 10 years, but inflation is incredibly low (2.5% US, 1.5% EU). In other words, even though you claim that the FED "gives asset holders free money", when you hold cash you're not really losing purchasing power. How do you square the two things?

Housing affordability crisis in nearly every urban centre.

In my view, QE's inflation happened before QE started. A significant purpose of QE was to prop up the loans made before the financial crisis. The inflation happened with the creation of trillions of dollars of securitized sub-prime housing loans. Rather than allowing those loans to default, the Fed is acting as a buyer of last resort through QE MBS purchases [0]. Without the Fed, much less money would be available for housing loans, and their prices would return to historical ratios to income [1, 2].

Absolutely, had I realized what the fed was doing when QE was happening I would have definitely done that. And a lot of people smarter than myself did do precisely that! Inflation is only “incredibly low” if you cherry pick the basket of goods used to measure it.

You're just running away from a complex thing you don't understand but has a lot of traction, to a simple thing which you understand but has no traction. My strategy is stick with the former and educate myself more. Different strategies.

Long term, you will either have government as we know it now, or an alternate currency, but not both. The monopoly on currency is closely related to the monopoly on force.

I generally think a lot of anarcho-capitalist theory to be obvious nonsense, but on that, they have a point.

The reason why you've never heard of it it's because it's not a huge boon to society. In the vast majority of cases it's an entirely pointless thing that you do just because you can.

I think that's a weak argument. All of the currencies listed in the article are limited to local purchases. At first glance they all seem to be paper money as well. They clearly solve none of the problems that concern crypto-enthusiasts/non-keynesians.

No, the reason I never hear about them is because they are limited in scope and simply defer power to another authority.

It's amazing that you are being downvoted for explaining exactly what Ben Bernanke himself said back in 2010. [0].

"This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion".

Pretty common for me to get downvotes for making a statement that goes against the hackernews groupthink. Then their comment throttle kicks in and I can’t post for a few hours and the groupthink can continue without interruption.

"That, in turn, should lead to higher spending in the economy.(1) The way in which QE works therefore differs from two common misconceptions about central bank asset purchases: that QE involves giving banks ‘free money’; and that the key aim of QE is to increase bank lending by providing more reserves to the banking system, as might be described by the money multiplier theory. This section explains the relationship between money and QE and dispels these misconceptions.

...

Two misconceptions about how QE works

Why the extra reserves are not ‘free money’ for banks

While the central bank’s asset purchases involve — and affect — commercial banks’ balance sheets, the primary role of those banks is as an intermediary to facilitate the transaction between the central bank and the pension fund. The additional reserves shown in Figure 3 are simply a by-product of this transaction. It is sometimes argued that, because they are assets held by commercial banks that earn interest, these reserves represent ‘free money’ for banks. While banks do earn interest on the newly created reserves, QE also creates an accompanying liability for the bank in the form of the pension fund’s deposit, which the bank will itself typically have to pay interest on. In other words, QE leaves banks with both a new IOU from the central bank but also a new, equally sized IOU to consumers (in this case, the pension fund), and the interest rates on both of these depend on Bank Rate"

If new money is created, and the new money is not distributed evenly among all citizens, all those citizens who receive less than an equal share are harmed while those who receive more than an equal share benfit.

It seems like the central bank, in this way, harms most people on a regular basis.

I am not prepared, however, to argue that Bitcoin is any better in this respect.

Well, I mean, the greatest economic booms in American history happened when our money was backed by gold. When the dollar came off the gold standard in the 70s, we saw wages decouple from productivity. This is not a coincidence.

Yes, and when there was free land available, and when the economy was small so growth was easier to achieve as a percentage, and when immigration was at levels that would be politically unthinkable today. So "This is not a coincidence" seems to be rather overstating the certainty of what the cause was.

Most people who claim that fiat money is essential for a growing economy are unable to explain the US economy from 1800-1914.

The real purpose of fiat money systems is so the government can spend more than it takes in by printing the difference (or the more modern variation of just creating it with accounting gimmicks).

The real point of fiat money is that it affords a government the option to increase the money supply at will.

Whether they do that for good (e.g. to attempt to combat a recession) or for evil (e.g. to invalidate government debt / inflate their way out of deficits) is a political exercise.

And knowing that, I actually think the US Fed is a pretty decent system. I shudder to think what would happen if Congress controlled monetary supply.

Second: incomes changed. The dollar worth alone is meaningless without lookiing at the purchasing power of the population. In 1800, a farm worker earned 12$ a month, which are $300 in 2018 dollars, so today's farm workers obviously earn more, regardless of the dollar's value. (source: https://babel.hathitrust.org/cgi/pt?id=wu.89071501472;view=1...)

I don’t think anyone claimed the value of a dollar was constant. Even on the gold standard there were periods of inflation and deflation. The average value over time was stable though.

> That's right, it averaged out to net zero over more than a century.

It just averages out because you selected an arbitrary period, which makes the point essentially meaningless. Id didn't average out from 1800 to 1900, from 1814 to 1914, from 1800 to 1850 and so on.

> It's a fundamentally different behavior, both in direction and magnitude.

Again, this is not correct. If you look at the actual data, you can see that the the inflationary periods in the 20th century actually have smaller inflation per year than those in the 19th century. The fundamental difference is the absence of severe deflationary crises, of which there were plenty in the 19th century. The top ten highest inflation rates of the last 200 years were all in the 19th century. Have a look at the data: http://www.in2013dollars.com/1800-dollars-in-2016

No, it wasn't stable. I have linked the actual data, please have a look. It was only stable if you select arbitrary time periods to make it look stable.

{kind=link}

Prof Richard Werner is worth listening to on this topic. [1]

I'd also recommend Steve Baker's heroic speech in UK parliament. [2]

[1] https://youtu.be/9bQkfN_pe44

[2] https://youtu.be/bXOkmD8Eozs