In the strange economy that this simulation proposes, every economic interaction is a zero-sum game. Some or all of the participants' money is placed in a pot and then randomly redistributed. This economy looks a lot like a poker tournament! As the game assumes that each economic interaction produces a winner and a loser, it is no surprise that simulation sorts the population into winners and losers.

I expect you'd find the same dynamics despite adding some positive externalities to the transactions. Depending on how large those externalities are. The nice thing about this example is the code is there for you to modify and test your theories.

A good simulation tries to pare down the system, not getting distracted by other mechanisms that don't change the basic dynamics. For example, it'd be more realistic if the transactions were partially parallelized, but that wouldn't change the analysis much.

Sure, there could be negative externalities as well. I think the complaint that the transactions were zero-sum implied that "real" economies increase total wealth with most transactions -- positive externalities.

The assumption that the economy was a zero-sum game was characteristic of the classical economists who came after Adam Smith. While Smith set himself the task of investigating the creation of wealth, his successors such as Ricardo, and notably, Malthus focused on the distribution of wealth.

During my PhD in economics, the first few quarters of microeconomic theory focused on what we call classical economics, which is also called partial and general equilibrium theory. These theories are definitely not zero sum games. Even though partial and general equilibrium theory don't describe economics in terms of interactions between individuals (in the classical theory, individuals interact with the market), if they did, the nature of these interactions would be that they are always strictly positive sum for all actors. E.g. consider the supply and demand curves, and imagine that for each vertical line (or horizontal, depending on how you draw the axes), you "match" the buyers and sellers along that line. Then the difference in the prices that each individual is willing to buy/sell for is the total gain for that transaction, with how the gain is distributed being determined by the equilibrium price.

Your summary seems to focus too much on early thinkers, and doesn't address the full development of classical theory which took until the 1950's.

Most post-Smith economics -- certainly everything in the market to tradition, classical or otherwise -- views normal transactions as net positive (and positive for each voluntary participant), not zero-sum.

But there's no reason to assume the degree of benefit is the same for each participant, and intuitively I think a more realistic net-positivr transaction rule with the gain randomly distributed would have distributionally similar results.

Ricardo was a paradigmatic case of non zero-sum thinking; he described comparative advantage, which shows the benefit of people specializing in different things.[1]

Some countries have less inequality, but also have less average wealth. People do not migrate to those poorer countries seeking to be richer than their neighbors. Instead, people tend to migrate to areas of higher wealth, even though it means they will have less relative wealth. It's clear that absolute wealth is more important to people than the zero-sum game of relative wealth.

1. By that logic, everyone who doesn't migrate from such a country is voting in favor of equality over absolute wealth and they constitute a much larger number.

2. To some degree, people do migrate to poorer areas and countries, including those of retirement age, to improve their perceived quality of life which is solely due to greater difference in wealth.

Australia 219,505

Luxembourg 182,768

Belgium 148,141

France 141,850

Italy 138,653

United Kingdom 111,524

Japan 110,294

Iceland 104,733

Switzerland 95,916

Finland 95,095

Norway 92,859

Canada 90,252

Netherlands 83,631

New Zealand 76,607

Ireland 75,573

Spain 63,306

Denmark 57,675

Austria 57,450

Greece 53,937

Sweden 52,677

Germany 49,370

Slovenia 44,932

United States 44,911

...

PS: US only has high wealth if you ignore debt. Owing 200k on a 200k house is not wealth.

There was some slight of hand on my part, the ratios are plotted, not the absolute numbers. The wealth inequality is more interesting than absolute country wealth in the context of the simulation I feel.

I agree regarding the debt, that's why net and gross values are included in the chart. For the top 3 it makes no difference. Iceland as an outlier isn't something I would have expected though

Edit: Also the mean probably isn't defined for whatever power law is generating wealth distribution in each country anyway

>Some countries have less inequality, but also have less average wealth. People do not migrate to those poorer countries seeking to be richer than their neighbors.

Of course they do. Retiring abroad in low cost locales is very common these days.

Wealth can be created or destroyed. Relative wealth has to operate in a sea of transactions that can either create wealth, destroy wealth, or, very rarely, maintain wealth.

In such a frothy environment how does the wealth of one entity hope to balance against all other wealth?

It is hard to say who gains more in a transaction.

What can be said is that in most transactions both parties walk away with more value. It is guaranteed to be a positive sum game -- value is guaranteed to be created.

The violation of this rule tends to happen if one or both parties will lose some value if they do not make the transaction, in which case they will try to minimize loss rather than maximize gain as measured by the value they entered the transaction with. This is the essence of exploitation.

These more varied classes of transactions can be a positive sum game -- where one party gets more value than the other loses, a zero sum game where they cancel out or a negative sum game where one gains less value than the other loses or they both lose but less than they would without the transaction having taken place. It is not guaranteed to be a positive sum game and value could be destroyed overall.

This simulation, where wealth is maintained at a steady state not only overall but within every transaction, is not really possible.

An important addition to this: it's usually only assumed to be a positive sum game at the time of the exchange and for the expected outcomes. It's very possible to see in retrospect that you wouldn't do the trade on a do over.

Asymmetric information, fraud etc.

Imagine that after each transaction, the measure of total wealth is normalized to have the original total. Whether or not actual wealth is increasing or decreasing, Norvig's simulation of nominal wealth will have the same dynamics.

How would you describe the value of being able to spend time with your children vs. being stuck far from your family? This is a trade parties could make, and could result in a Pareto improvement (e.g. if someone with no family traded jobs with someone who had children they loved).

One can generally convert all things to dollars. There's generally a price you can offer to convince someone to do most things, such as your example of spending time away from family.

Sure, money can't buy happiness, humans are weird about non-transitive preferences (if a is preferred to b and b is preferred to c, it turns out that sometimes c is preferred to a), and some things like ethics end up at infinite dollar value... but whatever, this is just a model. You can make it as complex/realistic as you think is necessary.

You're just restating what I said with just more words. But, you don't propose an alternative simulation model.

I would say that the simulation is actually generous. Wealth is correlated with power. Power creates opportunities for exploitation. I know of very few examples where this is not the case.

The alternative simulation model would allow transactions to create wealth or destroy wealth.

Wealth is correlated with power but that power is not necessarily only directed against other rational actors but the environment and circumstance, too. So it makes sense to see power as an increasing or decreasing value overall with time.

100% power in 1500 A.D. is very different than 100% power now (if percentage of power makes sense at all considering how dependent it is on circumstance).

The other thing about power is that there are power singularities. If I can cause the death or pain of another as part of a transaction either actively (gun to the head) or passively (they will starve without the transaction taking place), that person will spend almost any amount of value to avoid that fate. This kind of exploitation should be taken into account.

Power does not always, or even most of the time, create opportunities for exploitation. If someone has some base level of power to avoid the singularities as described above they can have transactions with more powerful entities that are not exploitative at all but of mutual value gained benefit.

Hitting a perfect zero sum game is a very simplified case and only useful as a rough approximation because most transactions are merely /close/ to zero sum with some value add otherwise the market would rush in to narrow the gap.

So, a more interesting model would take both the creation and destruction of wealth into account as well as the opportunities for exploitation (since, while those are not the bulk of transactions, in today's world they are still incredibly common).

This would be more interesting because it would show 1) how various levels power changes over time beyond the relative measure and 2) how prone each group is to exploitation.

If certain conditions lead to the lowest tier group having increasing power over time and reduce their exploitation potential but lead to large increases in the gap of relative power, that would be a much better outcome than if they have less overall power and are in more exploitable conditions but their gap of relative power is smaller, for example.

Economy is pretty much a zero-sum game. The non-zero-sum game part (growth) is very small (2-3% even if that) if you consider a country's economy (or world economy) as a whole.

I like to say if your income is consistently growing at ~10% every year, when the economy is growing at 2-3%, you're likely making someone worse off. (Although that someone might be some billionaire in which case have at it).

> I like to say if your income is consistently growing at ~10% every year, when the economy is growing at 2-3%, you're likely making someone worse off.

That is like saying, "The average age of the country is growing at 0.1% per year while my age is growing at 4% per year, therefore I must be making someone else younger." Income usually increases over the course of a career, but in the end, people retire or die and stop contributing to the average.

Wage-growth is conceptually different from the gains from trade within an economy. An isolated individual who doesn't trade(eg subsistence farmer) would produce goods of value of an order of magnitude less than current US GDP per capita.

Similarly, your hypothetical individual who 'makes someone worse off' must by definition be inheriting some scarce asset, be lucky, deceptive, coercive or inflicting negative externalities. Otherwise why would anyone trade with him?

This is not to say that inequality isn't a problem or greater redistribution would not be desirable. But you need to frame the problem correctly.

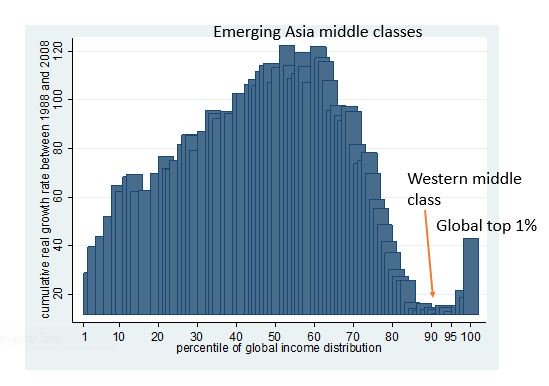

Seems like a wealth transfer from "developed country" workers to "less-developed country" workers and capital owners. The exact dynamics are of course hidden from that chart. The labels on the axes say that the peaks are gaining relative to the valleys in that chart.

No. There could be two phenomena occurring simultaneously: growth for everyone and layered on top of that a wealth transfer. The key term you're ignoring in my comment was relative: "peaks are gaining relative to the valleys".

I know you're into finance. Are you familiar with the concept of a long-short hedge fund? If so, you should be comfortable with the idea of focusing on relative movement of two assets within an asset class, hedging against the absolute movement of the asset class as a whole.

If you want to declare a delta between some hypothetical distribution and the actual distribution "wealth transfer", have at it. That is certainly irrefutable, albeit mathematically vacuous.

Not sure what you're getting at with "delta between some hypothetical... and the actual" but yes, I was describing something irrefutable. You'd asked what the chart meant. I looked at the axes labels and described the shape of the curve.

Middle class tends to rise off of the redistribution of rich class's wealth. Like I said, the second part of my original comment. (which is a good thing, so maybe "worse" is not the best word).

Nice to see this; it is often difficult to convey a complex point if you leave your audience to just imagine the outcomes.

A few months ago, I started looking into simulating economics while researching the housing situ in the Bay Area. I found that the NetLogo package is commonly used to simulate economics by sociologists.

It is interesting that the simulation in the linked article above treats the economic actors as aggregates, while the NetLogo simulation using many discrete actors is based on methodological individualism. It is easier in the second case to avoid the simple assumption that economic activity must necessarily be of a zero-sum nature.

I grew up in a very conservative environment and even now consider myself libertarian. Even so, a progressive tax plus a universal basic income just seem like the right way to put a floor on income on which people can stand and better themselves. The sim seemed a little abstracted from normal interactions, is there some equivalent simulation which shows what happens as we vary the progressivity of the tax code, and also vary the amount of a basic income?

Other questions: would it make sense to use the level of a basic income to stimulate the economy, rather than the fiscal stimulus to banks? Does a basic income or a progressive tax put a max on the wealthys' income in some non-obvious way, or just reduce it? Is there an economist who has applied control theory (i.e. the Kalman filter) to economics?

I did a similar simulation of income/wealth distributions using US income tax rates over the past century. It was a gloriously hackish combination of a Lisp tax-rate parser, auto-generated C actor model, and R.

I sure hope more economists study these methods because the standard models in Public Economics/Taxation are hopelessly inadequate, if not negligent.

A Nobel Memorial Prize winning economist by the name of James Mirrlees came up with a theory for optimum income taxation in the 1970s that is still used by governments today. It suggested that a relatively flat tax would be optimal rather than the progressive rates then in vogue. Unfortunately, his model is hopelessly incorrect as it essentially assumes that the general shape of the (pre-tax) income distribution is constant. Its starting point is that if you tax people too much, they will just work less than their untaxed income earning potential, hindering your ability to raise taxes.

In reality, progressive tax rates alter the ability of the wealthy to accumulate capital, which alters the Pareto coefficient (power-law constant) of the high-income tail, drastically changing the number of very-wealth individuals and benefiting the bottom 90%. If you tax too regressively, wealth can concentrate and even "condense" in the wealthy -- essentially shifting all earning capacity to a few. This happens because there exist power-law coefficients for high incomes that are not integrable. Beyond a tipping point, wealth will just continue to "condense" in the wealthiest actors.

You can find detailed tax schedules and inequality data for the US for the last century. The details of the actor-interactions are not that important, much like molecular interactions do not make a qualitative difference in statistical mechanics. In fact, analytical stochastic models may be easier to calculate, although they are less flexible.

Income tax progression can explain a large part of the variation, but not all. There are other important factors such as union participation, war-time expropriation, and lending terms. Nevertheless, the income tax schedule is important and easy to change.

I'd love to see some more details about this work, in a form like the OP's blog. Simulation results hold a big appeal to the HN crowd and I think you'd find a good audience for them.

Super interesting, and a not just a bit worrisome. I was reminded of how some ancient societies had periodic forgiveness of debts, perhaps one limited form of redistribution, though as we all know most societies historically have been made of a small wealthy minority lording over a mass of the poor...

The "transactions" might not have to be purely monetary for things to work out this way. We could include interactions where the winner gets privileges and status, later to be translated into economic wealth.

Btw Jupyter Notebook is so cool for things like this.

We still have debt forgiveness. It's called chapter 11 and bankruptcy. We still a wave of these every few years or so. The Asian financial crisis, dot com bust, GFC, and the latest wave of commodity producers going bust, are all prime examples of mass forgiveness of debts.

I'm curious as to why anyone would think economics could only be zero sum. How would they explain going from mud huts to skyscrapers and animals to aircraft? Such a "simulation" would not account for this obvious reality.

Transactions cannot be zero sum. What would the point be?

In the common case: Two people come together and trade because each feels they get more value after the transaction than before the transaction. Positive sum.

In a less common case: Two people get come together and trade because without the trade one of them would lose more than the value they spend on the transaction and the other one gains value. For example, if you have a gold watch but you are hungry and have no cash and I have food you might trade that watch for a sandwich. Also not a zero sum game. In this example a negative sum but I could imagine a positive sum where the one party gains more value than the other stands to lose after the transaction is complete. Say, you need to pay some workers on your construction crew and you have a generator that is normally worth about $50K and you sell it to me for cash at $40K. I, in turn, use that generator to do my job worth $100K that I wouldn't be able to complete without it..etc. It can get complicated.

A zero sum transaction would have one person losing the exact value the other person gains. A very odd and rare case I would guess.

Also gambling between two people - though one party loses the exact amount the other person gains, the time spent to place the bet and to watch the result costs time. One could argue they both gained utility in terms of enjoyment, but in terms of wealth and GDP the transaction is negative-sum.

By this logic any entertainment-related transactions are zero-sum. People gain utility by being entertained, sometimes you can even objectively measure it, e.g. higher productivity after holidays.

Note that you've made the leap from "may be" to "must be".

There are numerous highly persistent behaviors, including play, entertainment, sleep, drugs consumption, recreational physical activity in excess of all training response stimulus requirements, etc., which nonetheless continue.

While I'm not certain that all are beneficial, and I have a difficult time myself accepting certain of these, I suspect they play a useful and possibly even vital psychological role for those undertaking them.

Even explaining these as coping mechanisms for underlying pathologies isn't particularly satisfying.

Technological progress drives long term economic growth.

Economics merely tries to maximise utility of land, labor, capital. We already maximised utility of land and labor a long time ago. We can further increase that utility with physical capital (fancy word for possesion of technology).

<sarcasm>There is also financial capital (fancy word for money) and it's primary purpose is getting more financial capital. Buying land, labor or physical capital are secondary.</sarcasm>

This is really well presented and there are some surprising results. It would be good to add in gains from trade/interaction to the model.

Economic theory suggests that agents would not willingly consent to transactions with negative expected returns and there are plenty of examples of mutually beneficial transactions in the real world (most goods I buy I would have been happy to pay more and the shop makes a profit).

In this context, it would be interesting to see the tradeoff between efficiency and equality with different allocation rules (and resulting transaction frequencies). This could in some way relate to the optimal taxation literature....

Having known several economists, I've always wondered why these guys aren't rich, or at least better off than they are.

Economists understand the theories behind money and wealth creation much better than us but--as far as I've seen--they aren't richer than average university-educated people.

> Economists understand the theories behind money and wealth creation

Isaac Asimov was trained as a chemist before becoming a science fiction writer. He relates the story where someone asked him what kind of glue to use for gluing together certain materials. Asimov said he had no idea, and the person walked away shaking his head and presumably thinking "some chemist this guy is".

Understanding glues and adhesion is at least one level of abstraction higher than knowing fundamentals of chemistry.

Richard Feynman also had a great essay about how understanding quantum physics doesn't allow you to figure out everyday physics questions (eg., At what temperature does gold melt?). In theory it should be possible to derive the melting point of gold from quantum physics, but it's impossibly difficult to do so.

Likewise, creating wealth (doing business, trading stocks, etc.) is probably several levels of abstraction higher than knowing the theories behind wealth creation.

Unlike physics or chemistry, which has a heavy empirical backing and a degree of rigor in the application of logic, economics is founded on many axioms and assumptions which usually don't hold up to scrutiny and undermine the field's ability to make accurate predictions. The entire finance market was an ediface built on theories with the the assumption that prices arrive to some analytical equilibrium and describes nothing of how prices change over time. And in order to price derivatives, the Black-Scholes model ignores any statistical moments other than mean and variance. These abstractions get shakier the higher you go up.

Building abstractions when your foundation is questionable is building a house a house on sand. Don't be surprised when it collapses, as it did in 2008, and the spectre of wealth you perceive reveals itself as an illusion.

Regarding Isaac Asimov was trained as a chemist before becoming a science fiction writer. From his wikipedia article Around the age of 11, he began to write his own stories, and by age 19, after he discovered science fiction fandom, he was selling stories to the science fiction magazines. It would appear that his chemistry career came later.

I know a few who fit this description. They have very cogent reasons as to why that describes the group, but not themselves as individuals. It gets meta.

Can someone explain why the random_split (i.e. first) rule tends towards inequality? It seems that any time a rich&poor person meet, the expected outcome is that the poor person receives money -- E(Uniform(0, X+Y)) = (X+Y)/2 > min(X,Y). So how does that lead to a rich-get-richer effect?

If the pot is split at an random point between 0 and 1, then on average, 75% will go to one player and 25% to the other player. (It doesn't matter which player is which or how many points the players began the round with.) The equilibrium is a state in which the average pairing between two players is unequal in this 75/25 ratio.

Author says they were influenced by a class from Bard College. I will note that Bard is home of the far-left Levy Institute think tank.

It's hypocritical too, because institutions like Bard and UMKC are home to a lot of heterodox economists who rant and rave against the neoclassical orthodoxy for making unrealistic assumptions, and then they pull off rigged pseudo-Paretian chicanery like this. An economy of zero transaction cost spot-exchanging automatons without so much as a capital stock.

I would be interested to learn more about the class mentioned by Norvig, i.e. the economic modeling concepts presented by professor Sven Anderson in that class. I've been searching around but haven't yet found any journal papers, syllabus, etc.

Try adding capital stock and transaction costs. The code seems easy enough. See if that changes the outcome of your simulation. My experience is that the broad rich-get-richer dynamics remain the same.

I was simply listing them as non-present basics that even freshman Walras-Cassel equilibrium models might have. I can't just add a homogeneous blob of capital called K because that's subject to capital-theoretic criticisms and isn't how reality works (see Cambridge capital controversies, Ludwig Lachmann and GLS Shackle). I also can't bolt on transaction costs because those are variable and dependent on social institutions or fixed factors, such as property rights and geography.

There's no way I can encode a dynamic disequilibrating market process in this, and it'd be a fool's errand to treat models like this as having to say anything about real-world policy. Capital accumulation is far too dynamic a process to lead to rich-get-richer outcomes, anyway. See Capital and Its Structure (1956).

> it'd be a fool's errand to treat models like this as having to say anything about real-world policy

Then what kind of models should have something to say about policy? Simulations tend to emulate the observed phenomena of economies much better than traditional systems-of-equations models.

> There's no way I can encode a dynamic disequilibrating market process in this

Have you tried? There are plenty of easy examples in complex systems literature. We could probably find a simple non-linear mechanism to add to Norvig's model to make the equilibrium unstable. He's already got a bit of randomness, so the two combined would create dynamic disequilibrium. One of my favorite additions would be the possibility of catastrophic loss. Check out what happens to the dynamics when a transaction periodically results in the loss of all assets involved.

> Capital accumulation is far too dynamic a process to lead to rich-get-richer outcomes

That's a strange sort of statement. Are you saying this rich-get-richer phenomenon is an illusion or that because we can observe some counter examples one shouldn't make the rich-get-richer claim despite the general tendency? If the latter, that's like saying the stock market doesn't exhibit momentum because it sometimes changes direction.

A non-falsifiable situation is true of almost everything macro-economic, so you're sunk from the beginning. Might as well bow out of arguing that any of this is more than simple faith.

Probably my misunderstanding, but this simulation does not reflect a continued concentration of wealth in the hands of a few, in my opinion.

Please let me know your thoughts:

I agree that the concentration of wealth reflected in the charts shows that, at any point of time, the person at the 1st percentile owns an increasing fraction of the total wealth.

However, this same person is very likely to be almost immediately spoliated by the subsequent transaction, and give all its wealth to someone (maybe the poorest person).

In summary, there is a lot of social mobility, as can be revealed by commenting out the following line in the code (essentially, we now track the financial path of specific individuals, rather than the wealth of various percentiles):

def record_percentiles(population, percentiles):

#population = sorted(population, reverse=True)

N = len(population)

return [population[int(p*N/100.)] for p in percentiles]

So, it seems to me that, on average, everyone is equal over time, but each instant offers every participant dramatic ups and downs.

Am I reading the code correctly...two actors meet, pool their "wealth" or some portion of it and then that pot is redistributed in some way?

I guess it's interesting to simulate this to get a feel for how such a market system would work. It would be interesting to play around with a rudimentary system of taxation. Maybe something as simple as "take 10% from each pot and evenly distribute it among the poorest actors currently around" as a starting point.

Maybe it's because I randomly got interested in the French Liberals and am reading through "Economic Harmonies" but I'd be very interested in a model of "island economics". With a number of actors that have a list of preferences of items and only exchange if both are better of according to their list. In my mind it escalates quickly because I want to add the need to eat, production etc.

{kind=link}